Fake Loan Settlement Offers on WhatsApp How to Confirm Genuine or Fraud

Fake loan settlement messages on WhatsApp are a daily trap for stressed borrowers in India. The message sounds sure of itself, uses bank-like language, promises a big waiver, and makes you feel like you need to pay today to close your loan. Middle-class families fall for it because they are already under pressure from EMIs, recovery calls, losing their jobs, or medical bills. Small business owners fall for it because they don't have much cash flow and want to close the deal quickly to protect their reputation and operations.

Legals365 helps people check whether a loan settlement offer is real, safe, and legal. Advocate BK Singh says that WhatsApp settlement scams are a problem with documentation and authority, not with emotions. Advocate BK Singh says that there is only one rule: if the offer can't be verified through the right lender channels and the right written terms, it's not a settlement; it's a risk. Advocate BK Singh also teaches clients how to keep their money safe, their credit history clean, and how to avoid sending documents to people they don't know.

1. Why Loan Settlement Scammers Love Using WhatsApp

WhatsApp is quick, private, and easy to fake. Scammers make fake notices, copy logos, and use pictures of bank employees to scare people. Many scammers buy borrower data from unknown sources, which makes the message seem real because they know the type of loan you have, the name of the lender, and the amount you owe. They go after borrowers at night and on weekends when banks are closed, which makes it hard to check things out and leads to bad decisions.

According to BK Singh, the main weapon of the scam is urgency. Legals365 tells borrowers to take their time and check before they pay. Advocate BK Singh tells his clients to treat every WhatsApp offer like a stranger offering to lower your debt; they must be proven, not believed.

2. Common Signs That Almost Always Mean Fraud

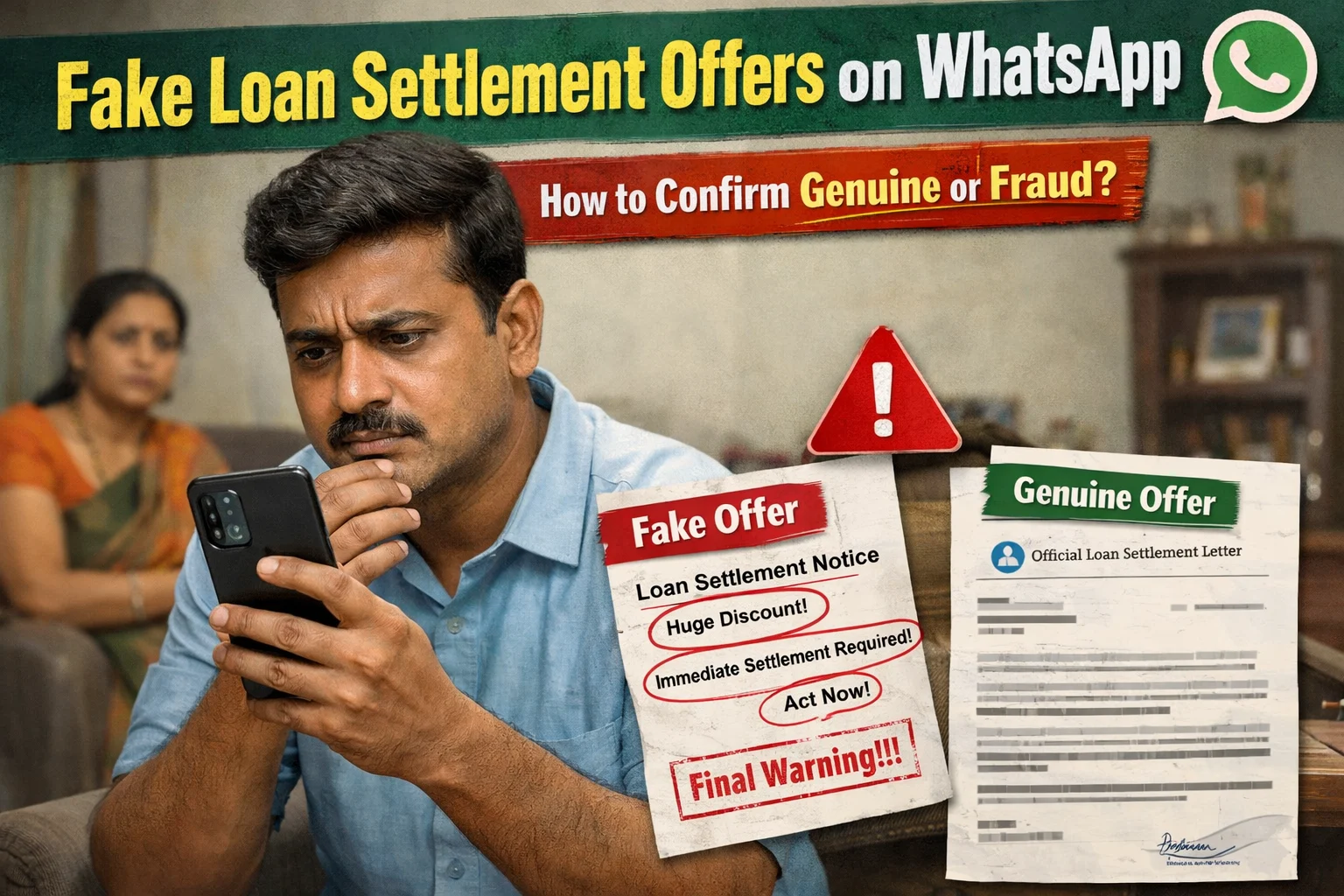

Some signs of trouble are very clear. They promise to settle everything at an unreasonably low amount without looking at your statement. Before they send you any official letter, they want you to pay a processing fee, filing charge, or stamp fee. They ask for payment through a personal UPI, QR code, or a private account name that isn't the same as the lender's. They won't give you their landline number or branch information, and they won't answer emails from an official domain. They want your OTP, card information, or net banking login.

Advocate BK Singh says that a real settlement is not a screenshot; it is a written offer sent through the bank system and properly received. Legals365 helps clients spot these warning signs early so they don't lose money twice: once to the scammer and again to the bank.

3. How a Real-Life Genuine Loan Settlement Usually Works

A real settlement is usually connected to your loan account and the lender's process. It usually includes a written settlement offer letter that lists the amount, payment date, method of payment, and conditions like the status of the case and the withdrawal of recovery action. You pay the lender using the approved account details, and you get a receipt and then a confirmation of closure or settlement. The bank keeps track of the terms of any negotiations that take place through written channels.

Advocate BK Singh helps clients understand the difference between talking about a deal and making a final offer. Legals365 helps people who are borrowing money ask the right questions before they pay. Advocate BK Singh tells clients over and over again that they shouldn't pay if they can't get a written offer that can be verified.

4. The Verification Checklist: Don't Pay a Single Rupee

Please ensure you verify these details before making any payment. Check the sender's name, title, branch, and official email address to make sure they are who they say they are. Request a settlement offer in the form of an official letter that includes the correct information about your loan. You can check for yourself by calling the lender's customer service number from an official source or going to a branch. Make sure the name on the payment account matches the name of the lender. Ask for a proper format for the receipt. Find out if your loan record will show that the settlement is settled or closed, and how the NOC will be sent. If the person doesn't want to be verified, treat it as fraud.

Advocate BK Singh sets up these checks as a simple script that borrowers can follow over the phone. Legals365 helps clients check letters and payment instructions. Advocate BK Singh also says not to send PAN, Aadhaar, bank statements, or selfies to numbers you don't know because using these documents in the wrong way can lead to bigger fraud later.

5. What should you do if you have already sent documents or made a payment?

Stop sharing documents right away if you already did so, and save screenshots of the chat. If you paid, get proof like a UPI reference, a bank statement entry, and messages where they asked for money. If you can, let your bank know right away so they can look into reversing the transaction. If you lose money, you should file a complaint with the cyber reporting system and also write a complaint at your local police station. Tell your real lender that you got a fake settlement message and ask for their official advice.

Advocate BK Singh helps victims put together a clean complaint pack with a timeline and evidence. Legals365 helps borrowers plan the legal steps without getting too stressed. In fraud cases, speed is important, so advocate BK Singh puts damage control first, then recovery steps.

6. How to make sure an offer is real when you're under pressure to recover

People who are under pressure to pay back loans are easy to take advantage of. People take shortcuts when they get recovery calls, threats of legal action, and stress from their families. The better way to do things is to make a proper hardship file and negotiate either directly or through a lawyer you know is good. A real settlement will stand up to scrutiny and not fall apart when asked simple questions. The lender won't mind if you check to see if the offer is real.

Advocate BK Singh tells his clients to keep all of their recovery information in one place, including statements, notices, proof of payment, and a record of all communication. Legals365 helps people who owe money write a clear request for settlement to the lender. Advocate BK Singh makes sure that the negotiation stays safe and doesn't lead to harmful admissions or payments that are too risky.

7. How scammers use the terms "NOC" and "account closure" in the wrong way

A lot of scams promise NOC. They say they will send NOC after payment, but they can't because only the lender can do that. Some scammers send fake NOC PDFs with logos and stamps on them. This makes things worse for the borrower when they try to use them to get a job or a loan in the future. Some victims think their loan is paid off because they got a message, but the bank account is still unpaid and interest is still accruing.

Advocate BK Singh says that only closure documents and receipts from the lender are important. Legals365 helps clients check with the real lender to make sure that the NOC is real and that the loan is closed. Advocate BK Singh's main goal is to protect your credit score and future eligibility. A wrong closure claim can ruin years of financial planning.

8. How Legals365 Helps You Check Offers and Keep Your Money Safe

Legals365 is a useful verification service that lets you check the sender's identity, the offer letter, the payment account, and the terms of closure. It also includes planning for safe negotiations so you don't fall for pressure tactics. This makes things clearer and less scary for middle-class families. It protects small businesses' money and reputation by keeping communication professional and on record.

Advocate BK Singh takes care of these things with strict verification rules. Legals365 makes a step-by-step plan for the borrower so they know what to do and what not to do today, as well as how to safely get real settlement terms. Advocate BK Singh makes sure that the process is clear and that any payment made can be tracked, received, and linked to real steps toward closure.

Client Reviews

*****

Nitin Aggarwal

I live in Delhi and got a WhatsApp message saying that my loan would close at half the amount. Advocate BK Singh looked over the letter and found problems right away. Legals365 helped me check with the lender, and I didn't lose a lot of money.

*****

Shweta Kapoor

I'm from Noida, and they asked for a processing fee first. I was going to pay. Advocate BK Singh helped me understand the verification script, and I saw that it was a scam. Legals365 helped me figure out a real way to negotiate.

*****

Faizan Khan

I live in Ghaziabad, and as a business owner, I needed the deal to close quickly. The scammer used this need for speed against me. Advocate BK Singh told me why urgency is a trap and helped me gather evidence. Legals365 made things clear for me and kept my money safe.

*****

Meenakshi Iyer

I live in Gurugram and sent my PAN and bank statement to a number I didn't know. Advocate BK Singh told them what to do right away and how to record the event. Legals365 helped me put together a good complaint package.

*****

Sandeep Verma

I live in Faridabad, and I already paid a little bit, but they wanted more. Advocate BK Singh told me how to keep chats and make the right complaints. Legals365 helped me get back in control and stop losing more.

?FAQs

Q1. How do fake loan settlement scams on WhatsApp work?

They promise a big discount settlement, make you feel rushed, and then either take your money as a fee or advance and disappear or keep asking for more.

Q2: Is it ever okay to make a settlement offer over WhatsApp?

A message by itself isn't enough. A real settlement needs written terms that can be checked, payment details that the lender has confirmed, and a receipt.

Q3. What is the most obvious sign that a settlement scam is happening?

A big red flag is when the lender's name on the payment request doesn't match the person's UPI or private account name.

Q4: Should I share my OTP or bank login to confirm the settlement?

Never. Sharing your OTP and login information is fraud and could lead to someone else taking over your account.

Q5. How can I tell if the person who sent it is a real bank agent?

Ask for the official email address, job title, and branch information, and then check with the lender's customer service or by going to the branch.

Q6. What papers should a real settlement offer have?

It should include information about the loan account, the amount of the settlement, the date of payment, the method of payment, the terms, and the process for confirming the settlement or closing the account.

Q7: What if I already gave money to a scammer?

Keep proof, tell your bank right away, file a cyber complaint, and write a complaint with a full timeline and proof.

Q8. Can scammers send fake NOC or closure letters?

Yes. A lot of people get fake NOCs. Always check with the lender to make sure the loan is closed and demand proper receipts.

Q9. Will settlement hurt my credit score?

A lot of lenders mark accounts as settled, which can hurt your credit score. Before agreeing to the terms, make sure you know how it will be reported.

Q10: How can Advocate BK Singh and Legals365 help?

Legals365 checks that offers are real, payments are safe, and the terms of the deal are clear. Advocate BK Singh helps with safe negotiation and how to deal with fraud.

There's no reason for concern. There is no difficult-to-understand legalese.

Someone who has helped many people with the same problems gives you clear, honest advice. We want to make the legal process easy to understand and use for everyone.

+91-9625961599 Chat on WhatsAppSchedule Your Consultation