India's economy now relies heavily on electronic payment systems like UPI (Unified Payments Interface), NEFT (National Electronic Funds Transfer), RTGS (Real Time Gross Settlement), ECS/NACH (Electronic Clearing Service/National Automated Clearing House), and online card transactions.

As digital payments become more common, there are more cases of failed or dishonored transactions, which can have legal consequences, especially when there isn't enough money or credit. An electronic payment that was not honored is one that could not be completed, like a bounced check. The Information Technology Act, 2000, the Negotiable Instruments Act, 1881, and the Payment and Settlement Systems Act, 2007, along with guidelines from the Reserve Bank of India (RBI), cover these kinds of situations in Indian law. Below is a full list of the civil and criminal penalties that come from dishonored electronic payments, as well as the differences that can be made based on the situation and the options available to those who have been wronged.

Electronic Payment Methods and the Laws That Apply

India's legal system treats electronic payment instructions the same as traditional ones, which means that digital transactions are legally valid and can be enforced. Important modes and how the law treats them are:

UPI, NEFT, RTGS, IMPS, and other bank transfers are all electronic funds transfers between banks. The Payment and Settlement Systems Act, 2007 (PSS Act) says that all of these kinds of transfers are "electronic funds transfers." Section 2(1)(c) of the PSS Act says that "electronic funds transfer" includes any transfer of money that starts with an electronic instruction to a bank. This includes online banking, mobile payments, point-of-sale transactions, ATM transfers, and more. So, if UPI payments or NEFT/RTGS transactions fail because there isn't enough money, the PSS Act (explained below) can be used against them.

ECS/NACH e-Mandates: These systems let creditors (like lenders and utility companies) take money out of a payer's bank account on a regular basis. Section 25 of the PSS Act says that an ECS or NACH debit that doesn't go through (like an EMI auto-debit that "bounces" because there isn't enough money) is a dishonoured electronic funds transfer. This clause was added to make the treatment of bounced checks for electronic mandates the same.

Card payments made online are also considered electronic fund transfers under the PSS Act. In practice, if you try to use a debit card when you don't have enough money in your account, the transaction will usually be declined right away, so you won't have to deal with a dishonored transaction later. Transactions that go over the credit limit on a credit card are also turned down. Real-time declines usually mean that the payee doesn't have to pay any debt, but if a recurring card payment or a delayed settlement fails because of credit limits, it could fall under the PSS Act's scope. "Exceeds the amount arranged to be paid" covers situations where credit limits are breached. In general, though, card networks make sure that the payee (merchant) isn't left unpaid in an authorized transaction. The liability shifts to the card issuer and, ultimately, the cardholder, who must then repay the issuer. So, dishonor in the card context usually means that the cardholder is liable to the issuer in a civil case (and may have to pay penalty fees) instead of directly dishonoring a payee.

The Negotiable Instruments Act, 1881 (NI Act), which makes it a crime to bounce a check, mostly applies to paper instruments (checks) and some digital versions of checks. The NI Act was changed to cover "cheques in electronic form" (signed with digital signatures) and electronic images of truncated cheques. But the NI Act doesn't consider purely electronic payment instructions, like UPI transfers or ECS mandates, to be "cheques." The PSS Act of 2007, on the other hand, governs the dishonor of these kinds of payments. The Information Technology Act, 2000 adds to this framework by making electronic records and digital signatures legally valid, making sure that electronic payment instructions and authorizations are also legally valid and enforceable. The IT Act also has rules about cyber crimes (for example, the IT Act or IPC can punish fraudulent or unauthorized online transactions), but these only apply in cases of fraud, not just when payments don't go through.

Criminal Responsibility for Failed Electronic Transactions

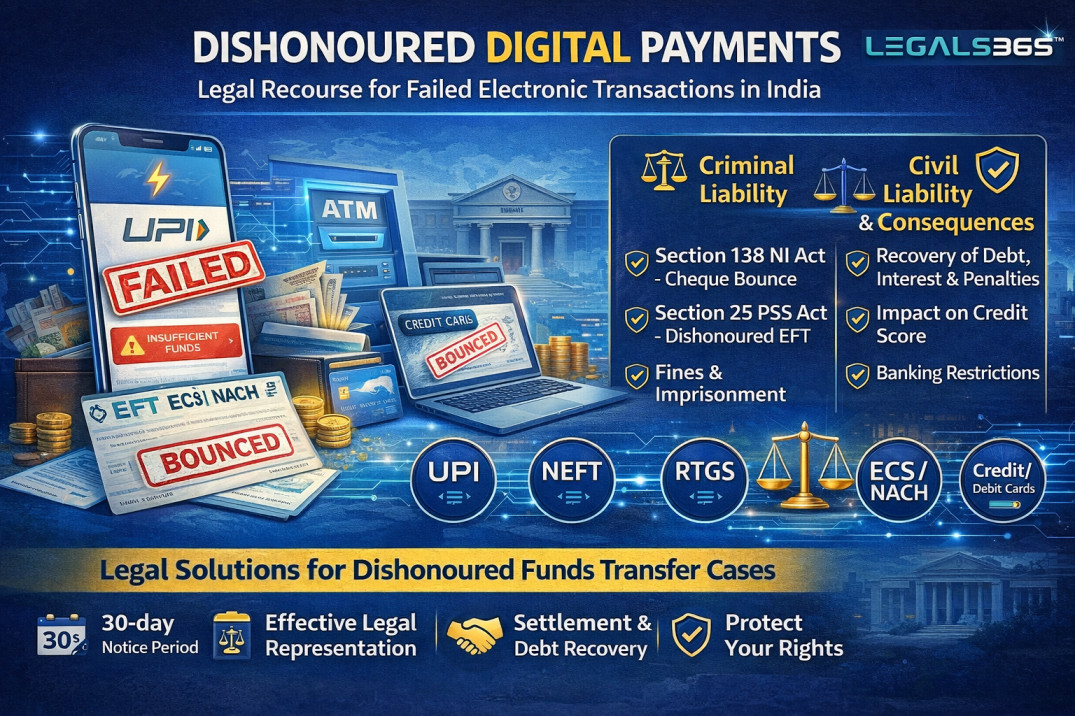

1. Cheque Bounce: Section 138 of the Negotiable Instruments Act says that it is a crime to dishonor a check because there isn't enough money in the account. Section 138 says that if a person or business writes a check to pay off a debt or liability and it is returned unpaid because there isn't enough money in the account (or because it goes over an agreement with the bank), the person who wrote the check could go to jail for up to two years and/or pay a fine that is twice the amount of the check. The law says that the payee must send the drawer a written demand notice within 30 days of getting the bank's cheque return memo. The payee must then give the drawer 15 days to pay. You can file a criminal complaint in the magistrate's court if you don't pay by that date. These rules apply to people and also to businesses (where officers in charge of the business's affairs can be vicariously liable under Section 141 of the NI Act). Mens rea (criminal intent) is not a necessary component; even if the drawer asserts ignorance or lack of intent, it typically does not serve as a defense under Section 138 once the technical criteria are satisfied. The act of issuing a dishonored check is enough to be guilty of the crime (the Supreme Court has said that the accused's reason to believe the check would be honored doesn't matter).

2. Dishonour of Electronic Funds Transfer – Section 25, Payment and Settlement Systems Act, 2007: The PSS Act makes a similar crime to deal with problems with electronic payments. Section 25 of the PSS Act makes it a crime if a person tries to send money electronically (EFT) but can't because they don't have enough money or because it goes over the bank's credit limit. The punishment is the same as in the NI Act: up to two years in prison, a fine of up to twice the amount of the failed transfer, or both. This makes it a crime to bounce electronic payment instructions (like ECS debits, UPI auto-debits, etc.) in the same way that it is a crime to bounce checks. But for this crime to happen, some conditions must be met.

Debt or Liability: The EFT must have been made to pay off a legally enforceable debt or liability, either in full or in part. This means that casual money transfers that aren't backed by an obligation wouldn't be considered a crime.

Procedural Compliance: The payment must have been started in line with the procedural rules of the payment system in question. For instance, an ECS mandate or UPI mandate must be set up correctly according to NPCI/RBI rules. This remedy may not be available for an EFT that doesn't follow the right steps.

Notice of Dishonour: The payee must send a written notice to the payer within 30 days of getting word from the bank that the payment was not made. In short, when the payee finds out that the electronic payment instruction didn't go through (for example, they get a failure message or return memo), they have to send a demand notice, just like they would in a case of a bounced check.

Failure to Pay after Notice: The payer does not pay within 15 days of getting the notice of dishonor. A criminal complaint can only be filed after this grace period ends. (This 15-day period gives you a chance to fix an honest mistake or make other payment arrangements before you become legally responsible, similar to the NI Act's plan.)

If these conditions are met, the person who is owed money can start a criminal case. Section 25(5) of the PSS Act makes it clear that the rules in Chapter XVII of the NI Act, 1881 (Sections 138–147) "shall apply" to dishonor of electronic funds transfers as far as the situation allows. In other words, the same legal protections and options that are available for bounced checks are also available for electronic payment dishonors. This includes presumptions in favor of the payee (for instance, the law presumes the EFT was initiated for a debt/liability, unless proved otherwise, just as Section 139 of NI Act presumes a cheque is for discharge of liability) It also means procedures like interim compensation to the payee (Section 143A NI Act) and appeal deposit requirements (Section 148 NI Act) equally apply to EFT dishonour cases The RBI has clarified that Section 25 of the PSS Act offers “the same rights and remedies that are available in Section 138 of the NI Act” for beneficiaries of electronic payments.

Dishonoring electronic mandates has been tried in court, for example. In Ritu Jain v. State (2019), the Delhi High Court ruled that dishonoring an ECS electronic payment is a crime under Section 25(5) of the PSS Act, just like bouncing a check. More recently, NPCI (which runs UPI) issued guidelines to strengthen this system. For example, UPI AutoPay (the UPI e-mandate feature for recurring payments) is now covered by Section 25. A November 2021 NPCI circular confirmed that if a UPI AutoPay transaction (like an EMI payment to a lender) fails because there isn't enough money, the lender can "seek remedy available in case of cheque bounce" under Chapter XVII of the NI Act, read with the PSS Act. This is because NPCI required these transactions to use a specific merchant code for loan/EMI to make this possible. This extension gives merchants and lenders a strong legal way to deal with intentional or careless defaults on digital payments, just like the cheque bounce system.

3. Other Criminal Provisions: In addition to these specific laws, some situations may fall under general criminal laws:

Indian Penal Code (IPC): If a payment that wasn't honored is part of a bigger scheme to cheat, the person who made the payment could be charged with cheating (Section 415/420 IPC) or criminal breach of trust (Section 406 IPC) in addition to or instead of the NI Act/PSS Act charges. For instance, if someone sends a fake payment confirmation or starts a payment they never meant to make in order to trick the payee, they can be charged with cheating.

Information Technology Act Offenses: If someone dishonors an electronic payment by messing with computer systems or stealing someone's identity (like using someone else's UPI ID or a cloned card), the IT Act, 2000 makes it a crime to steal someone's identity (Section 66C) or cheat by pretending to be someone else using computer resources (Section 66D). These are not about the dishonor itself, but they do talk about how digital payment systems are being used fraudulently.

It is important to remember that to bring IPC or IT Act charges, you have to show that the person who didn't pay had dishonest or fraudulent intent, not just that they didn't pay. The NI Act and PSS Act offenses, on the other hand, are simpler ways to deal with bounced payments. They don't require proof of intent and are often called "strict liability offenses" to keep people financially responsible.

Civil Liability and Other Results

A failed electronic payment means that the debt or obligation is still not paid. The person who was wronged (the payee) can still get the money back through civil means, even if there is a criminal case. Some important civil liabilities and consequences are:

Getting the Money Back: The person who owes the money can file a civil suit to get the amount owed back, plus interest and any penalties that are part of the contract. The payee can file a summary suit under Order XXXVII of the Civil Procedure Code for a faster judgment if the obligation came from a contract or written agreement, like a loan agreement or an invoice. Even if the instrument was electronic and not a traditional negotiable instrument, civil proceedings can still be used to enforce the underlying liability. The courts can give the principal amount plus interest for the delay.

Penalties and Fees in Contracts: It's common for loan or credit contracts to say what happens if you don't pay on time. For example, loan agreements often charge a "bounce charge" every time an ECS mandate or check is not honored. The borrower is legally responsible for these fees, which could be a flat fee or a percentage of the payment. Banks also usually charge fees for failed auto-debits or returned checks from the account holder. These fees are not "legal penalties," but they are direct financial results of the dishonor.

Interest and Late Fees: In addition to one-time bounce fees, the person who owes money may have to pay interest on the amount that is late (especially if it is a credit card or loan). If an automatic payment from a bank account fails for a credit card bill, the card issuer will charge late fees and interest until the bill is paid. The cardholder agreement makes these things possible.

Credit Score Impact: Credit bureaus can be told about repeated or serious missed payments, even if they are fixed later. A record of ECS or check dishonors (especially on loans or credit cards) can lower a person's credit score, making it harder for them to get a loan in the future. For businesses, these kinds of defaults could hurt their credit score or trade reputation. This isn't a legal liability in and of itself, but it's something that banks and other financial institutions keep an eye on, and it can encourage people to keep their payment promises.

Business Relationships and Contracts: If a business doesn't keep its payment promises (for example, if its digital payments to suppliers bounce), it could lose business relationships, have to pay damages, or have its contracts canceled. Suppliers might want you to pay in advance or make the terms stricter. In some cases, if a company can't pay its debts, persistent defaults can even lead to bankruptcy proceedings against it.

Banking Restrictions: The RBI says that banks can take action if someone doesn't pay their bills on time. The Reserve Bank of India (RBI) has told banks to have rules for punishing people who don't pay their bills on time. For example, if a customer's checks or ECS mandates keep bouncing, the bank can send them warnings and even stop their checks or ECS services. If a customer repeatedly refuses to pay, banks may close their accounts or refuse to offer certain services. This is a rule that the bank has to follow because the RBI told them to in order to stop people from abusing the system.

Finally, it's important to remember that if the bank or system is to blame (and not the payer), the payer or payee may be able to sue the service provider. For instance, if a bank wrongly denies a valid payment (for example, it freezes the account by mistake or a technical error causes a transaction to fail), and this hurts the payee or damages the payer's reputation, the person who was hurt could ask for compensation. Consumer protection laws say that if a bank wrongfully dishonors a payment when there are enough funds, it is a "deficiency in service." In these cases, the bank has to pay the customer for any loss or damage to their reputation. The RBI's banking ombudsman has also looked into complaints like these and found them to be service problems.

Liability and Differences Between Individuals and Businesses

Individuals and businesses (corporate entities) can both be punished for not honoring electronic payments, but the law works differently for each:

Companies can be held criminally responsible: If a company (or any other legal entity) pays, it can't go to jail, but it can be fined. More importantly, the people in charge of the company's money can be held personally responsible. Section 141 of the NI Act (which is included in the PSS Act through Section 25(5) says that anyone who was in charge of and responsible for the company's business at the time of the crime is guilty of the crime. If a private limited company's check bounces or its ECS payment fails, the managing director or finance manager who signed or approved the payment can be charged with a crime. They may be able to defend themselves by showing that they didn't know about the crime or that they did everything they could to avoid it, but the law puts the burden on them at first. (Partners in a partnership firm or office bearers of an association can also be held responsible for the firm's unpaid bills.) There are also ways to sue the company itself for fines. This makes sure that the corporate form can't be used to avoid paying debts.

Individuals: An individual (or sole proprietor) who makes a payment that is not honored is directly responsible. The proceedings are in their own name, and they could be fined or sent to jail. There is no separation of liability like there is with businesses. But sometimes a person will try to avoid responsibility by saying they didn't know or it was a mistake. As we said, these defenses usually don't work, but courts can be sympathetic in real cases of unintentional technical errors.

Reputation and Compliance: For businesses, not paying on time can have bigger effects. If a company misses a lot of payments, it might get in trouble with regulators or lose its relationships with banks and lenders. For example, if a company's ECS loan payments often bounce, banks might lower the amount of credit they give the company. Some companies are also required to report financial obligations and defaults (for example, public companies must report major loan defaults). A single bounced transaction may not necessitate reporting; however, recurring instances of non-payment could. On the other hand, someone's unpaid bills mostly hurt their credit and can lead to lawsuits, but they don't usually lead to regulatory action unless they are very big (unless the person is a professional borrower or has a lot of lawsuits, in which case law enforcement may look into fraud).

Intentional vs. Operational Lapses: A dishonored payment in a business could sometimes be due to operational problems (like cash flow timing or an employee not paying attention) instead of the top management's deliberate choice. Companies often have internal checks to stop defaults because they know the legal and reputational risks. If someone is the only one in charge of their account, they can only blame themselves for not keeping money in it. Section 138 of the NI Act/PSS Act says that both are equally responsible, but a court might take into account any mitigating factors when deciding on a sentence. For example, a court might be a little more lenient if a small business missed a payment because it was short on cash but paid right after getting the notice, instead of in a case of fraud. Even so, the law's letters apply to everyone in the same way; the differences are more about how things work than the law.

Intentional Default vs. Technical Failure

It's very important to figure out what caused the dishonor. The law mostly goes after people who don't have enough money or credit (which means the payer is in default), not people who fail because of technical problems or bank mistakes. So, the effects can be different:

Intentional or Negligent Default: The law holds the payer strictly liable if they knowingly make a payment that will not clear or if they are careless in not keeping enough money in their account. The classic example is writing a check when you know you don't have any money in your account or letting an ECS/UPI debit go through on an empty account. The criminal laws (NI Act/PSS Act) are meant for these kinds of situations. They put pressure on people who owe money to be responsible with their money and not send payment orders they can't honor. Section 25(3) of the PSS Act makes it clear that saying "I thought I had funds" is not a defense once dishonor is proven. This is because the payer "had no reason to believe" there would be insufficient funds. So, the law punishes people who intentionally or carelessly break the rules to stop them from doing it again. Also, people who break the law more than once may be watched more closely (for example, a history of bounced payments might make a magistrate give a harsher sentence or a bank cut back on services).

Technical Problems and System Bugs: Not every failed transaction is the fault of the person who paid. There are times when a payment doesn't go through because of technical problems, like when the network goes down, the bank's servers have a bug, or the payment system has bugs. In these situations, the failure is not because there isn't enough money, so it doesn't fall under the Section 138 NI Act or Section 25 PSS Act. The laws only apply when the payer's account is empty or over the limit. A technical failure is basically the same thing as a service failure. In this case, the solution is usually operational and civil: the banks are expected to reverse any wrong debits and finish the transaction or tell the customer to try again. The RBI has put rules in place to protect customers in these situations. For example, if an ATM withdrawal or UPI transfer takes money out of your account but doesn't give you the cash or the beneficiary doesn't get the credit, the bank has to automatically reverse the transaction within a certain amount of time (usually T+1 or T+5 days, depending on the channel). If they don't, they have to pay the customer for the delay. These rules make sure that customers aren't unfairly punished for technical problems. From the payee's point of view, a technical failure means they haven't received the money. They can just ask the payer or the system to start the payment again once the problem is fixed. There is no criminal intent, so there is no criminal case. If the payee loses money because of the delay (for example, if they miss a deadline), they may be able to sue the responsible institution for any damages they can prove.

Grace in Real Mistakes: There can be gray areas. For example, a payer thought there was enough money in the account, but a delay in another transfer meant there wasn't enough money at that exact moment, which led to dishonor. This is technically a crime, but the law's process (the notice period) gives you a chance to fix it. No prosecution will happen if the payer pays right away (within 15 days). Sometimes, courts have thrown out cases where the default was truly technical or unintentional and the amount owed was paid. This is because they see the criminal process as being for people who willfully default rather than for minor or honest mistakes. The law tries to tell the difference between dishonest or careless non-payment and innocent technical failures by giving a notice and cure period. However, each case is different.

If someone knowingly sends a fake payment screenshot or uses a hacked system that is likely to fail, that is a type of fraud. In these situations, police can use cybercrime and fraud laws in addition to the NI/PSS Act, as mentioned earlier. When deception is involved, intentional default becomes fraud, and the penalties can be harsher (including jail time under IPC/IT Act rules that are separate from the payment laws).

To sum up, the law punishes dishonors for not having enough money, but it does not treat technical failures as crimes; instead, it treats them as service or operation problems that need to be fixed. This balance is important for encouraging digital payments because it protects users from technical problems and punishes those who don't pay on purpose.

What the Payee Can Do to Fix the Problem

If an electronic payment is not honored, the person who was supposed to get the money has a number of options:

Demand Notice: The first step for both checks and electronic transfers that are meant to pay a debt is to send the payer a written demand notice. The notice should tell the payer that the payment has been dishonored and ask for the full amount due, which usually includes any interest or fees that apply. If you want to take criminal action under the NI Act and PSS Act, you must send this notice within 30 days of finding out about the dishonor. A formal notice serves as proof of the demand and can sometimes make the payer want to settle the matter privately, even if there is no criminal case.

Criminal Complaint (Cheque or EFT Bounce): If the person who owes money doesn't pay within 15 days of getting the notice, the person who is owed money can file a criminal complaint under Section 138 of the NI Act (for a bounced check) or Section 25 of the PSS Act (for a bounced electronic transfer). A Judicial Magistrate (First Class) or a Metropolitan Magistrate will hear the complaint. The payee (or their lawyer) needs to show proof of the transaction, the dishonor (like a bank's return memo or failure report), the notice, and the lack of payment. If the drawer is found guilty of a crime, they may be punished, and the defaulter usually pays up quickly (to make things worse and avoid jail). Some courts may also order that some of the money from fines be used to pay for damages. It's important to remember that criminal prosecution has a time limit. The complaint must be filed within a month of the event that caused the action (i.e., the day after the 15-day notice period ends without payment).

Civil Litigation for Recovery: The payee can seek civil remedies at the same time as or instead of criminal action. You can file a civil suit to get a decree for the amount owed (with interest). In a lot of cases, people who owe money choose the criminal route to put pressure on the other party and to get a settlement faster, since civil suits can take a long time. But civil lawsuits always have a clear outcome because they are only about getting money back, not punishing the defendant. It is common to do both: file a Section 138/Section 25 complaint and then file a civil suit or use arbitration if the contract allows it. If the debtor still won't pay, winning a civil suit will let the payee get their money back through court processes, like attaching the debtor's property. Also, as was said before, Order 37 summary procedure is available in civil court for debts based on instruments and written contracts, which speeds up the case.

Alternative Dispute Resolution: If the payment that wasn't made was part of a contract that has an arbitration clause (which is common in business contracts), the person who was supposed to get the money can take the case to arbitration. Many loan agreements, for instance, have a clause for arbitration in case of defaults. The arbitrator can give an award for the amount that hasn't been paid. Arbitration is a civil remedy that can be used instead of going to court. It doesn't have the punishment part of criminal law, but it can help the debtor get back on their feet if they have assets.

If a bank's services are at fault, like if the payee didn't get the money because of a bank mistake or the payer's bank won't help them get dishonor documentation, they can file a complaint with the RBI Integrated Ombudsman, which handles complaints about banking and digital payments. The Ombudsman can tell banks to make up for mistakes, like when a bank's carelessness caused a payment to be lost or a refund to be delayed. This way is more about getting money back from financial service providers than from the person who paid, and it's helpful if the bank or system is to blame or not working with you. It's a free, fast way for customers to settle disputes.

Direct negotiation and settlement: When a payment doesn't go through, the parties may be able to work things out without going to court. The payee could just tell the payer and get another payment (another transfer, cash, etc.) to settle the debt. Even if a legal notice is sent, the person who owes money may pay within the notice period, which stops the police from taking action. In India, courts strongly encourage people to settle cheque bounce cases. If the person who bounced the cheque pays the amount and any agreed costs, complaints are often dropped even at later stages. So, from a practical point of view, one important "remedy" is to use the threat of legal action to get someone to pay. After payment, the immediate problem goes away (though the default may still make the trust between the two parties weaker).

Other Options: Consumer Forum: If the payee is a consumer and the payment that wasn't made causes them to lose money, they might also want to file a complaint with a consumer forum. For instance, picture this: a person makes an electronic payment to a store, but it doesn't go through, and the store cancels a service or booking, which costs the person money. If the payment service provider or bank was at fault, the person (as a customer of banking services) might be able to get money back for bad service. This is not the most direct way to deal with dishonour situations, though. It usually happens when a service provider clearly fails (like when a bank wrongfully dishonours a payment).

In short, the law has two ways to get people to pay on time: criminal pressure (with the threat of jail time) and civil processes (with interest or damages). The payee can choose which way to go based on the situation. People often use the criminal complaint as a strategy because the threat of criminal charges often makes a defaulter want to settle and pay. On the other hand, civil judgments are very important if the person who owes money can't pay or won't pay even after criminal charges (because criminal courts don't automatically make the person who owes money pay the amount of the check to the person who complained unless it's part of a fine or settlement). In all cases, the person who is wronged needs to have proof of the transaction, the failure, and the notice in order to win in court.

Important Case Law and Precedents

For decades, Indian courts have dealt with payments that weren't honored under the NI Act for checks and more recently under the PSS Act for electronic payments. Some important legal precedents and points are:

Ritu Jain v. State (Delhi High Court, 2019) was an important case that showed that dishonoring an ECS electronic mandate is a crime under Section 25 of the PSS Act. The court noted that Section 25(5) of the PSS Act makes the whole Chapter XVII of the NI Act (Sections 138–147) apply "to the extent circumstances allow" for electronic dishonors. An ECS mandate bounce was treated the same as a bounced check, and the petitioner (who wanted to stop the proceedings) was not given any relief. This showed that the PSS Act mechanism worked.

Clarification from the RBI: The RBI's Chief General Manager made a statement around 2010-2011, when electronic payments were on the rise, to make it clear that Section 25 of the PSS Act gives beneficiaries "the same rights and remedies" as Section 138 of the NI Act. This was done to clear up any confusion in lower courts that may not have been aware of the new PSS Act provisions. So, complaints about electronic transfers that weren't honored should be handled in the same way.

Case of UPI Mandates: We expect to see enforcement in cases where UPI AutoPay mandates fail after NPCI's 2021 notification. This is an area that is still growing. It fits with other ECS cases, but the technology is different because e-mandates through UPI are new. It will be interesting to see if any of the decisions mention UPI failures by name. So far, they would logically follow the same rules as ECS/NACH cases, as long as the mandates were set up correctly under NPCI rules (MCC 7322 for loan payments, etc., as required).

Frequent Dishonour Policies: It's not case law, but it's interesting that the RBI told banks to take action against customers who frequently dishonour cheques or ECS after a Joint Parliamentary Committee suggested it after the stock market scam in the early 2000s. A lot of banks, like SBI and others, now have rules for their own employees. For example, if a customer bounces three checks in a year, they get a warning. If they bounce a fourth check, their checkbook may be suspended or their account may be closed. Repeated ECS mandate failures get the same treatment. This isn't "law" in the sense of the law, but it is a regulatory consequence that the RBI has the power to enforce. It makes it clear that the system does not take repeated payment failures lightly.

The Supreme Court has made it clear in Dashrath R. Rathod v. State of Maharashtra (2014) and Rangappa v. Sri Mohan (2010) that the purpose of Section 138 NI Act is to make negotiable instruments more trustworthy by punishing dishonor. The same idea applies to electronic payments through the PSS Act. Courts have also said that mens rea is not necessary for Section 138 because the crime is more like a regulatory crime. Some people have said that this is too harsh, but it is still the law. At the same time, the criminal courts often encourage compounding (settlement) because they know that the goal is to get paid, not to go to jail. Changes to the NI Act in 2018 added Sections 143A and 148 to make the payee's position even stronger (with interim compensation and deposit on appeal). These changes also apply to PSS Act cases.

Recent Precedents: The court used the NI Act and the PSS Act in the case of State Bank of India vs. Ashwani Kumar (2024, reported in some forums) to deal with a dishonored ECS mandate. It is said that the rules in Chapter XVII of the NI Act were used for an ECS from an SBI account, which shows that the approach is consistent. In a trial court case called Intec Capital Ltd. vs. Rajiv Kumar (2025), an ECS mandate bounced. The court ruled that the legal notice and complaint were valid under Section 138 of the NI Act and Section 25 of the PSS Act for the ECS default. These cases show that both higher and lower courts are hearing electronic dishonor complaints, which means that payees have options and that these laws are being used.

Consumer Court View: When banks wrongfully dishonor a check, consumer courts have found banks responsible. If albank makes a mistake and doesn't follow a standing instruction or a NEFT, which causes the customer to miss a payment, the bank can be ordered to pay for the loss as a result of bad service. This doesn't make banks legally or criminally responsible, but it does set a precedent in consumer law that they need to be careful when processing payments.

This article does a great job of explaining dishonored digital payments in India in a way that is easy to understand. It explains UPI, NEFT, RTGS, ECS/NACH, and card payments in detail, and then it talks about what happens when these payments don't go through. It is very easy to understand the difference between technical failure and not having enough money, as well as the link between Section 138 of the NI Act (cheque bounce) and Section 25 of the Payment and Settlement Systems Act, 2007 (EFT dishonour).

The article is very helpful because it talks about both criminal and civil consequences. It tells readers about notice periods, deadlines, court procedures, RBI rules, how defaults affect credit scores, and how banks and businesses respond to repeated defaults. It also gives the payee real, useful ways to fix the problem, like notice, complaint, civil suit, arbitration, ombudsman, and settlement, instead of just talking about theory. In general, it seems like a full legal guide for anyone who has had a UPI/ECS/NACH/auto-debit or check bounce problem, whether they are a person borrowing money, a small business, or a big company.

What Legals365 and Advocate BK Singh Can Do for You

Legals365 and Advocate BK Singh deal with these kinds of problems all the time, like bounced checks, ECS/NACH payments, UPI AutoPay failures, EMI defaults, and loan settlement disputes. They help both payees (people who are supposed to get money) and payers (borrowers or customers who are under pressure to pay back their debts).

For people who owe money, lenders, or businesses

Writing strong legal notices for bounced checks and dishonored EFTs under Section 138 of the NI Act and Section 25 of the PSS Act.

Going through all the paperwork (invoices, loan agreements, mandates, and bank memos) to see if a criminal case is possible and how strong it will be.

Filing and handling complaints about bounced checks and dishonored electronic payments in the right court, as well as filing or helping with civil recovery suits when necessary.

Negotiating safe settlements and terms of compromise so that money is really recovered and not just a case filed on paper.

Making settlement deeds and court compounding applications to wrap things up neatly once the payment is received.

For people who are paying or borrowing money and are being harassed or recovering money

Looking over notices and messages from banks, NBFCs, and recovery agents and giving a clear legal opinion on how big the real risk is.

Writing polite but firm responses to legal notices that point out technical problems, banking mistakes, or disputes over who is responsible when they apply.

Making realistic repayment or settlement plans (part payment + installments) and putting them into a legally binding settlement so that the harassment stops and the risk of going to jail is as low as possible.

Handling court cases that have already been filed (Section 138/Section 25 complaints), looking for bail, compounding, and closing cases when possible.

Giving advice on how to avoid defaulting on loans again, how credit affects future loans, and how to avoid defaulting again.

Advocate BK Singh and the Legals365 team deal with loan defaults, bounced checks, NACH/ECS bounces, UPI AutoPay, and digital payment disputes every day. They know both the technical banking side and the courtroom side.

For payees, getting their money back faster and legally.

For payers, a legally safe end with the least amount of harm to life, business, and reputation.

Amit, Jaipur (Matter handled in Dwarka Court): *****

I was anxious because a NACH payment to my vendor bounced and I received a formal notice. The advice helped me understand timelines and reply properly. I felt real relief after getting clarity and closing it professionally.

Neha, Lucknow (Matter handled in Tis Hazari Court): *****

Our small business had an EFT mandate bounce dispute with a customer. The process was explained in simple language, and the documentation was organised well. I finally felt in control instead of panicking.

Rohit, Indore (Matter handled in Karkardooma Court): *****

I didn’t even know ECS dishonour could become a legal issue. The guidance helped me arrange my bank proofs and communication properly. Outcome-wise, the matter moved towards settlement without unnecessary drama.

Shabana, Patna (Matter handled in Rohini Court): *****

I received a notice mentioning Section 25 PSS Act and got very stressed. The approach was calm and practical—what to reply, what to keep ready, and what mistakes to avoid. That clarity reduced my fear.

Vivek, Chandigarh (Matter handled in Patiala House Court): *****

Our service dues were pending and the client’s mandate kept bouncing. The documentation and notice strategy were handled carefully. I appreciated the balanced, professional way the situation was managed.

There's no reason for concern. There is no difficult-to-understand legalese.

Someone who has helped many people with the same problems gives you clear, honest advice. We want to make the legal process easy to understand and use for everyone.

+91-9625961599 Chat on WhatsAppSchedule Your Consultation