Chargeback, RBI Complaint, and Police Case Flow for Credit Card Fraud

In India, credit card fraud has changed. In the past, it was either a stolen card or a simple OTP scam. Now, there are skimming at gas stations and point-of-sale machines, token theft through hacked apps, card details leaking from merchant systems, and "card-on-file" misuse, where the card is never physically touched. Three international transactions can happen in five minutes on a middle-class salary account. A small business owner can lose money with a corporate card and also have problems with vendors when payments are blocked. The worst part is the pressure loop: the bank says "customer authorized," the merchant says "we delivered," and the victim has to prove that they didn't do anything wrong.

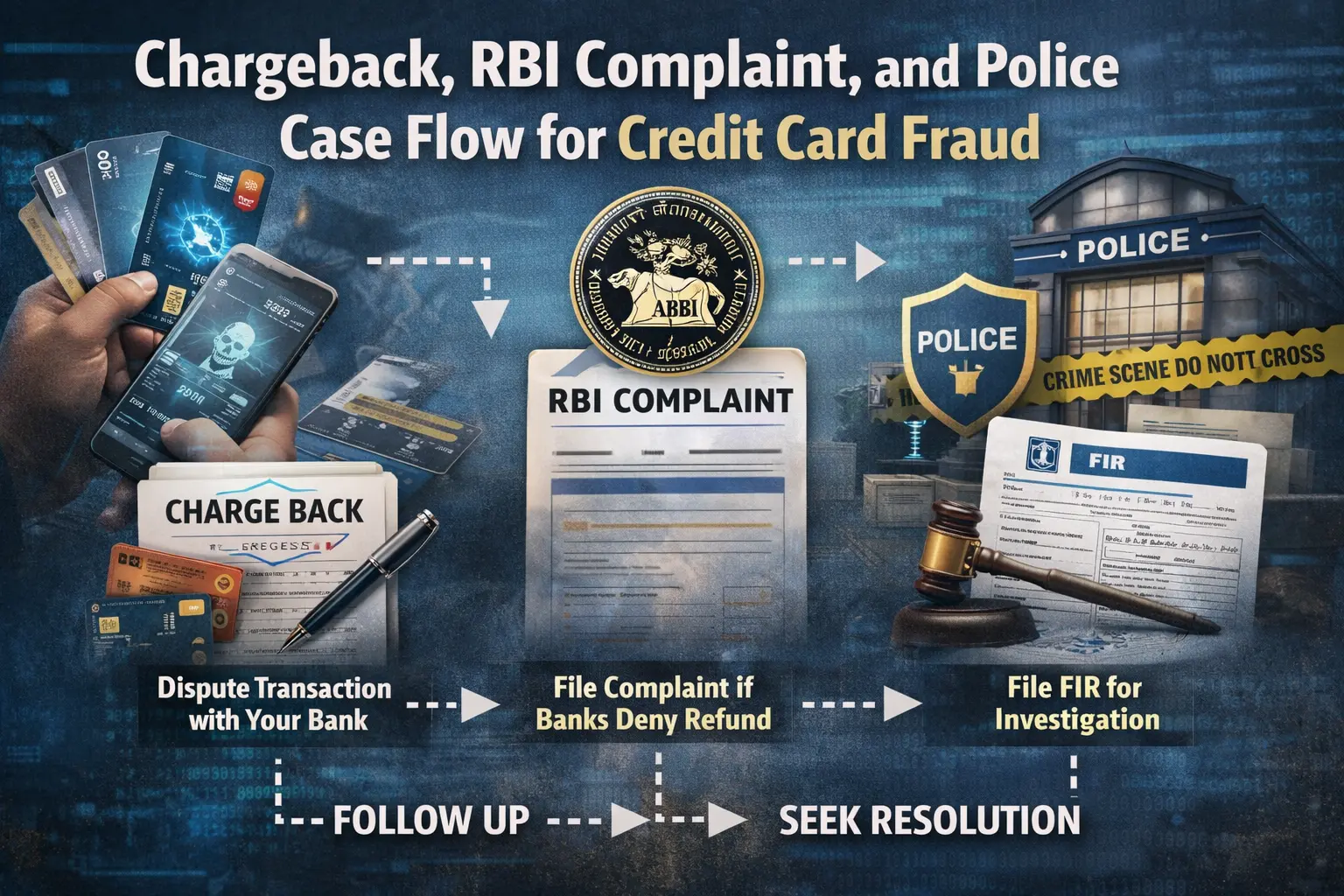

Advocate BK Singh runs Legals365, which handles these cases as a recovery and defense process, not as a lecture. The goal is clear: block the card right away, start a dispute, follow network rules for chargebacks, escalate complaints to the RBI if banks take too long, and create a police or cyber case file that supports reversal and stops future abuse. In real life, the order of events is more important than how fast they happen. The bank ends the dispute if the file is weak. If the file is organized, reversals and interim credits are possible.

1. What a real-life case of credit card skimming or token theft usually looks like

Most victims see it in one of three ways. First, they get a text message about a transaction they never made, usually for e-commerce that is international or worth a lot of money. Second, a lot of small "test" debits, and then one big transaction. Third, an EMI conversion or merchant subscription that the cardholder never agreed to. Skimming cases are often linked to recent card swipes at busy retail counters, gas stations, or restaurants. Token theft and card-not-present fraud often happen after someone gets access to your email or phone, clicks on a suspicious link, or gives an app permission.

For small businesses, it often means employees using shared devices or company cards to pay for travel and vendors. Because the statement due date is coming up and the bank wants payment even though the dispute is still open, fraud becomes a cash flow problem. Advocate BK Singh and Legals365 say that the first step is to limit the damage, and then they will build a case that can stand up to standard "authorized transaction" replies.

2. Why chargeback is often the fastest way to get your money back

Police action is important, but when a transaction is made with a credit card and a merchant acquirer is involved, chargeback is the best way to get your money back. The chargeback system uses proof and reason codes. A disagreement that is explained in an emotional way but not backed up by facts often fails. A dispute that shows non-delivery, unauthorized card-not-present use, duplicate processing, wrong currency conversion, or a merchant not following authentication rules has a better chance of being resolved.

Legals365 gets disputes ready in the language that banks use to process them, including transaction IDs, timestamps, merchant descriptors, device and location mismatches, and the exact type of dispute. Advocate BK Singh's approach is evidence-first because chargeback teams make decisions based on what can be proven, not what hurts.

3. The right "first day" file that makes banks pay attention to you

Banks respond more quickly when the first complaint packet is neat. The strongest early file usually has screenshots of transaction alerts, a written dispute email to the bank's card disputes channel, confirmation of card blocking, and a short, factual account of what happened. If the fraud is connected to a merchant interaction, like swiping a credit card at a gas station or restaurant, the time and place of the swipe are important because they support the skimming claim.

A common error is to wait for the next statement. That delay gives merchants time to settle their debts, which makes it harder to get the money back. On the first day of the dispute, Legals365 helps clients set it up and makes sure that all of the acknowledgment numbers, reference IDs, and bank emails are kept in one place. Advocate BK Singh keeps the language strong and professional so the bank can't take it lightly.

4. If the bank takes too long or closes a dispute, you can file a complaint with the RBI.

In a lot of real-life situations, the biggest battle isn't with the fraudster; it's with the delay. Some banks keep disputes "under process" until the payment is due, which puts pressure on the customer. Some people end disputes with a standard line like "transaction authenticated," even if the cardholder never got an OTP or used the card.

When there is a service failure, a delayed response, a denial without a proper investigation, or harassment through recovery calls during an active dispute, RBI escalation becomes important. Legals365 writes the escalation in a way that makes it clear where the bank's timeline is missing and includes the dispute trail in a clear way. Advocate BK Singh uses escalation as a way to put pressure on the bank, not as a decoration, so they know that the case is being handled professionally.

5. Police and cyber case flow that helps you get your money back and keeps you safe

A police report is not just for catching the bad guy. It also makes your case more believable, especially when banks ask for a "proof of fraud" document. The complaint should include the type of fraud, the card number masking, the transaction details, the suspected source if known, and the steps taken right away, like blocking the card. It should also ask for action to find beneficiary merchant accounts and device trails when they are available.

Legals365 makes sure that the police report and the bank dispute don't conflict with each other. Advocate BK Singh says that consistency is important because if there is one difference between the police statement and the bank dispute, the bank can use that as an excuse to turn down the request.

6. How to realistically prove skimming and token theft

People who have been skimmed often ask, "How can I prove it?" Pattern, timing, and mismatch all work together to make proof. If the card was used in person at one place and then online or internationally within a short period of time, that mismatch makes it easier to compromise. The pattern gets stronger if more than one victim reports the same fraud at the same merchant point. If the device, IP address, or authentication mode is different from what you usually use, that becomes important.

Legals365 helps you organize your case by showing the recent swipe timeline, your location, proof that you owned the phone, and the fact that you reported it quickly. Advocate BK Singh doesn't overpromise. He makes a file that looks real and can stand up in court, which is what really wins chargebacks and escalations.

7. Common arguments made by banks and how a strong legal file can refute them

When you talk to a bank, they usually say things like "transaction successful," "PIN used," "OTP verified," "merchant settled," or "customer responsibility." A strong file doesn't get upset about these lines. It fights back with evidence of mismatches, quick reporting, logic about transaction patterns, and a demand for proper investigation records. It can also call into question the bank's internal controls, especially if the transaction looks risky but wasn't flagged.

Stopping late fees, stopping recovery pressure, and getting temporary credit while the case is being worked on are all helpful for middle-class families. For small businesses, it's all about keeping working capital safe and making sure that payments to vendors stay steady. Legals365 is all about these real results, and Advocate BK Singh keeps the dispute strategy focused on getting results that can be recovered, not on courtroom drama.

8. How Legals365 and Advocate BK Singh deal with credit card fraud cases from start to finish

Credit card fraud is a three-step process: a bank dispute and chargeback, an RBI level escalation for service failures, and a police or cyber file for criminal action and proof. When these tracks don't align, the victim finds themselves in a loop. When the parties are in agreement, the bank takes the dispute seriously, paving the way for recovery.

Legals365 helps clients with structured dispute drafting, chargeback documentation, escalation representations, police complaint alignment, and follow-ups that are meant to stop harassment and increase the chances of getting the money back. Advocate BK Singh's method is professional and based on evidence. It focuses on quick control, clear paperwork, and practical recovery outcomes for small businesses and middle-class families.

Reviews from clients

*****

Aarav Mehta

After a normal swipe, my card was skimmed, and within hours, there were transactions in other countries. Legals365 made the chargeback file correctly, and the bank finally saw it as fraud. Advocate BK Singh stuck to the facts, and it became clear how the reversal process worked.

*****

Sana Qureshi

I never agreed to a lot of online payments that were made after a token was stolen. Legals365 helped me organize my dispute trail and stop recovery pressure while the dispute was still open. The team of Advocate BK Singh took it seriously and didn't treat it like a normal complaint.

*****

Rohit Bansal

I own a small business, and right before my payment was due, someone charged my business credit card without my permission. Legals365 made sure that the bank dispute and police complaint didn't conflict with each other. Advocate BK Singh's plan kept my cash flow safe.

*****

Neha Kapoor

At first, the bank closed my dispute because they said it was allowed. Legals365 took it to the next level with the full record, and the case was reopened. The bank acted more quickly and responsibly because of Advocate BK Singh's writing.

*****

Imran Siddiqui

A fake merchant transaction was made to look like a real one. I didn't waste time arguing on the phone because Legals365 took care of the chargeback logic and follow-ups. Advocate BK Singh's method seemed solid and focused on getting results.

?FAQs

Q1. What does it mean to skim a credit card in India?

It is stealing card information through hacked swipe machines or point-of-sale systems, which is then used for transactions that aren't allowed.

Q2. What does it mean to steal tokens in credit card fraud?

It is wrong to use stored payment tokens from apps, devices, or merchant systems to make payments without the card itself.

Q3. Can I get a chargeback for credit card transactions that I didn't authorize?

Yes, if the dispute is filed quickly with the right paperwork and the transaction meets the requirements for a chargeback.

Q4. How long do I have to report a fake card transaction?

Right away. Fast reporting makes chargebacks stronger and also helps stop more abuse and limit liability.

Q5. Do I need to file an FIR for credit card fraud?

It is highly advised, particularly for substantial sums, recurrent fraud, or when the bank necessitates a police report to facilitate reversal.

Q6. What if the bank says an OTP or PIN was used?

If you never got an OTP or never made the transaction, a structured dispute should ask for investigation records and point out patterns of mismatches.

Q7. When should I make a complaint to the RBI?

When the bank takes excessively long, closes disputes without providing a valid reason, persistently harasses you during an active dispute, or fails to meet service deadlines, it's time to file a complaint with the RBI.

Q8. Can late fees and interest be stopped while a dispute is going on?

In many cases, banks may stop charging or give temporary relief based on the facts and how they handle policies.

Q9. What should a small business do if someone uses a corporate card fraudulently?

You should block the card, keep proof of the transaction, promptly raise the dispute, file a police report, and ensure that the accounting records accurately reflect the dispute.

Q10. Why should you use Legals365 for disputes related to credit card fraud?

With Legals365, you can handle chargeback drafting, RBI escalation, and police complaint alignment all in one plan. Advocate BK Singh's main focus is on practical recovery and protection.

There's no reason for concern. There is no difficult-to-understand legalese.

Someone who has helped many people with the same problems gives you clear, honest advice. We want to make the legal process easy to understand and use for everyone.

+91-9625961599 Chat on WhatsAppSchedule Your Consultation