How to File a Cheque Bounce Case in India

A practical legal guide by Legals365 for individuals, professionals, landlords, lenders, traders, and businesses dealing with dishonoured cheques in India.

A cheque bounce problem often begins with trust and ends in stress. Someone promises payment, issues a cheque, and assures you that the amount will clear without issue. You deposit it in good faith. Then the bank returns it unpaid. Now you are left dealing with delayed money, excuses, business pressure, and legal confusion. In many cases, people wait too long because they do not know the proper process. That delay can cost them valuable legal rights.

If you are trying to understand the Best Cheque Bounce Case in India, the first thing you need to know is that a successful case does not depend only on anger or financial loss. It depends on speed, documentation, correct legal notice, proper filing, and careful strategy.

Under Section 138 of the Negotiable Instruments Act, a dishonoured cheque can lead to criminal prosecution if the cheque was issued for a legally enforceable debt or liability, the statutory notice is sent within the prescribed time, and the drawer still does not pay within 15 days of receiving that notice. The complaint must then be filed within the legal limitation period before the proper Magistrate court.

This is where many people make mistakes. They rely on informal calls. They send a weak WhatsApp message instead of a proper legal notice. They file in the wrong court. They fail to preserve bank documents. Or they assume that once the cheque bounces, the case is automatically strong. It is not automatic. A strong cheque bounce case is built properly from day one.

At Legals365, clients usually come with the same practical questions. Can I still recover my money? How much time do I have? What documents matter most? What if the other side claims the cheque was only a security cheque? What if the cheque amount is large and the person keeps delaying? These are not small issues. For many individuals, traders, landlords, suppliers, consultants, doctors, transport operators, and small businesses, a bounced cheque affects cash flow, credibility, and peace of mind.

The law gives a remedy, but procedure matters. The cheque must be presented within its validity period. After dishonour, the payee must send a written demand notice within 30 days of receiving the bank return information. If the drawer does not pay within 15 days of receiving the notice, the cause of action arises, and the complaint should ordinarily be filed within one month thereafter. Jurisdiction also matters and is linked to where the cheque was presented for collection in the manner described by Section 142.

In plain language, filing a cheque bounce case in India is not just about proving that the cheque failed. You must show that the cheque was issued toward a real liability, that you followed the legal timeline, and that your paperwork supports your version clearly. A good cheque bounce lawyer helps you do exactly that. A smart legal team does not simply prepare a complaint. It builds pressure lawfully, anticipates defence arguments, and positions the matter for recovery, settlement, or conviction depending on what the case requires.

This guide explains the complete process in a clear and practical way. It is written for people who want real answers, not textbook theory. Whether you are a business owner dealing with unpaid invoices, a lender trying to recover dues, a landlord facing default, or a professional who was handed a cheque that bounced, this article will help you understand how the process works in India and how Legals365 can support you at every stage.

Why cheque bounce cases are taken seriously in India

A bounced cheque is not merely a banking inconvenience. In many situations, it reflects a failed payment obligation. Indian law treats it seriously because cheques are meant to carry commercial credibility. When people issue cheques casually and then avoid payment, the damage goes beyond one private dispute. It affects trust in business dealings and everyday financial transactions.

Section 138 of the Negotiable Instruments Act exists for this reason. It creates penal consequences when a cheque issued for a legally enforceable debt or liability is dishonoured and the drawer still does not pay after receiving the statutory demand notice. Punishment may extend to imprisonment up to two years, or fine up to twice the cheque amount, or both.

That said, the law does not work on emotion. Courts look at facts and compliance. If you miss the notice period or file too late without proper justification, even a genuine grievance can weaken badly. This is why people searching for the Best Cheque Bounce Case in India should focus less on dramatic claims and more on legal precision.

What qualifies as a cheque bounce case under Section 138

Not every dishonoured cheque becomes a valid Section 138 prosecution. Certain legal conditions must exist.

First, the cheque must have been issued for a legally enforceable debt or liability. If there was no genuine liability, the matter can become contested. Second, the cheque must be presented within the prescribed validity period. Third, it must be returned unpaid by the bank. Fourth, the payee or holder in due course must send a written demand notice within 30 days of receiving information from the bank about dishonour. Fifth, the drawer must fail to make payment within 15 days of receiving that notice. Only then does the cause of action to file the complaint arise.

This means a cheque bounce case is not complete on the date of dishonour alone. The legal notice stage is built into the cause of action. If you skip that stage or handle it casually, you may damage the case before it starts.

Common real life situations where cheque bounce cases arise

Cheque bounce litigation is far more common than many people think. It appears in both personal and commercial settings.

A supplier delivers goods to a retailer. Payment is partly made by cheque. The cheque bounces due to insufficient funds.

A landlord receives a rent cheque from a tenant after repeated delays. The cheque is dishonoured.

A friend borrows money and issues a cheque for repayment. When deposited, it comes back unpaid.

A contractor completes work for a business client and receives a post-dated cheque. The project ends, but the cheque bounces.

A property transaction gets stuck. One party issues a refund cheque. The cheque fails.

A business partner tries to buy time by issuing multiple cheques, hoping the other side will not pursue the matter seriously.

In all these cases, the legal strategy depends on records. Messages, invoices, account statements, agreements, acknowledgment of dues, and bank return memos can all matter. Many clients assume the cheque itself is enough. In reality, surrounding documentation often decides how strong the case looks when the other side starts denying liability.

Best Cheque Bounce Case in India: what actually makes a case strong

People often use the phrase Best Cheque Bounce Case in India as if it means the biggest claim or the most aggressive legal notice. That is not how strong cases are built. A strong case usually has five qualities.

Five things that make a cheque bounce case stronger

- A clear liability trail through invoices, settlement notes, messages, ledger, or written acknowledgment.

- Procedural discipline in cheque presentation, legal notice, and complaint filing within limitation.

- Document consistency between cheque amount, return memo, notice, and complaint.

- Service proof showing the demand notice was dispatched and served or deemed served.

- Strategic handling of likely defences such as security cheque, denial of debt, or signature misuse.

In many recovery matters, the case becomes strong not because the facts are dramatic, but because the file is clean.

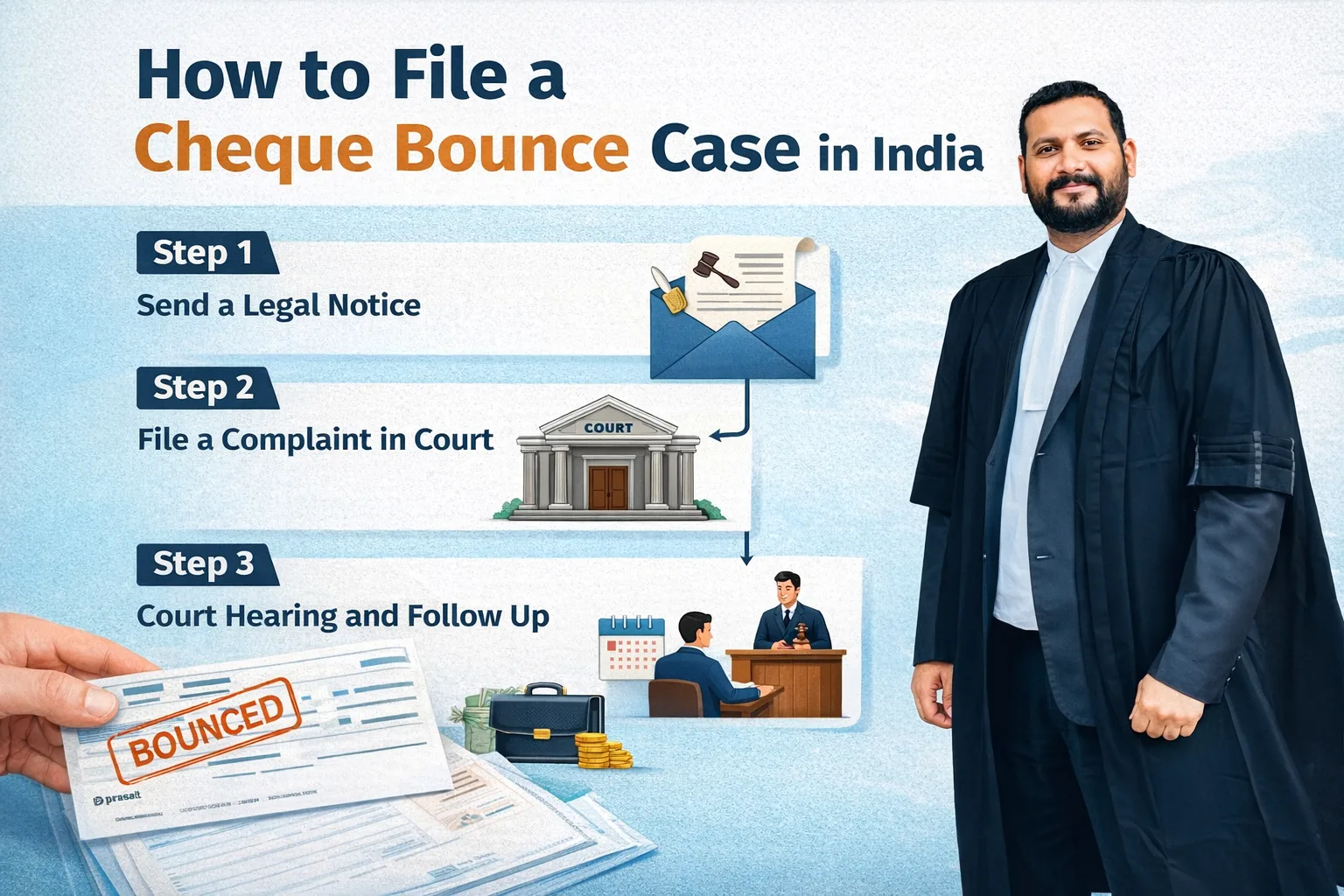

Step by step process to file a cheque bounce case in India

Start by depositing the cheque within its validity period. The Negotiable Instruments Act refers to presentation within six months from the date of the cheque or within its validity period, whichever is earlier. In practice, banks now typically honour the shorter operational validity reflected in banking practice, so immediate presentation is always safer. The practical point is simple: do not sit on the cheque.

If someone tells you, “Wait a few weeks, then deposit it,” be careful. Delays can complicate your legal position and give the drawer more room to create confusion.

If the cheque is dishonoured, the bank issues a cheque return memo stating the reason, such as insufficient funds, payment stopped, account closed, or exceeds arrangement. This memo is one of the most important documents in the case. Preserve it carefully.

Do not rely only on a bank SMS or verbal information. Ask for the official return memo and keep copies. Your legal notice and complaint will refer to this document.

This is the point where delay hurts most. Many people spend two or three weeks calling the other side, hoping for settlement, and then approach a lawyer after the notice deadline is nearly over. That is a mistake.

A cheque bounce lawyer can quickly review your dates, check whether Section 138 applies, identify supporting documents, and draft a strong statutory notice. Quick review matters because the notice must go out within 30 days from the date you receive information from the bank regarding dishonour.

At Legals365, this early-stage review often makes the difference between a routine filing and a properly positioned recovery case.

The legal notice is not a formality. It is the legal trigger. Section 138 requires the payee or holder in due course to demand payment through a written notice within 30 days of receiving intimation of dishonour from the bank.

What a proper legal notice should mention

- The cheque details

- The date of presentation

- The dishonour information

- The amount due

- The nature of the liability

- A clear demand for payment

- A reasonable description of the transaction

- The legal consequence of failure to pay within 15 days

Weak notices create trouble later. Overstated allegations, wrong dates, inflated demands beyond the cheque liability, and poor service proof can all damage the case. For related support, see cheque bounce notice legal services and how to draft a legal notice for cheque bounce.

Once the drawer receives the notice, the law gives them 15 days to make payment. If payment is made within that period, the criminal cause of action under Section 138 does not survive. If payment is not made, your right to file the complaint arises after expiry of those 15 days.

This period often becomes a negotiation stage. Some people call and seek time. Some offer part payment. Some deny everything. Some avoid notice service and hope the matter dies. A disciplined legal team keeps proper records of all responses and decides whether to settle, extend commercial time, or move ahead firmly.

After the 15-day period expires without payment, the complaint should ordinarily be filed within one month from the date the cause of action arises. Section 142 governs this stage and also allows the court to take cognizance after the prescribed period if sufficient cause for delay is shown.

This is another place where genuine claimants lose cases. They assume that because they already sent the notice, they can file whenever convenient. That is wrong. Limitation still matters.

Jurisdiction in cheque bounce matters is governed by Section 142(2). Broadly, if the cheque is delivered for collection through an account, jurisdiction attaches to the branch of the bank where the payee maintains the account. If presented otherwise, the location of the drawee bank branch can become relevant under the statutory framework.

Jurisdiction questions should never be guessed. Filing in the wrong court causes delay and unnecessary objections.

Your complaint should clearly explain:

- Who issued the cheque

- Why it was issued

- How liability arose

- When it was presented

- How it was dishonoured

- When notice was sent

- How notice was served

- How payment was not made

- Why the court has jurisdiction

Supporting documents usually include the original cheque, return memo, copy of legal notice, postal receipts, tracking proof, and transaction records. Depending on the case, invoices, ledger accounts, emails, WhatsApp chats, loan acknowledgment, settlement terms, and bank statements may also help.

If the complaint appears properly made, the Magistrate may take cognizance and issue summons to the accused. Then the litigation begins formally.

At this stage, many drawers suddenly become serious. Some who ignored calls for months become ready to negotiate once summons arrive. This is why early procedural accuracy matters. A weakly built matter gives the other side comfort. A clean case creates pressure.

Section 138 cases can still settle at various stages. Mediation and compromise are often explored in appropriate matters. Courts have also recognized settlement avenues in cheque bounce disputes.

But settlement should be structured carefully. If you agree to part payment, instalments, or compounding terms, get the terms recorded properly. Never close a live case casually on mere assurance.

Documents required to file a cheque bounce case

One of the biggest myths in these matters is that only the bounced cheque matters. In reality, document quality shapes the outcome. A standard file may include:

- Original cheque

- Bank return memo

- Copy of legal notice

- Postal receipt or courier proof

- Delivery report or tracking record

- Reply to legal notice, if any

- Invoices or bills

- Ledger statement

- Loan acknowledgment or handwritten undertaking

- Rent agreement, if the matter relates to rent

- Emails, messages, or chats acknowledging payment

- Bank statement showing relevant transfer history

- Identity and address details of the drawer if available

Legals365 also highlights the importance of proper documentation for proving a cheque bounce case in court. You can link this section to documents required for a cheque bounce case.

If you run a business, keep invoice numbers, delivery proofs, purchase orders, GST records, and statement of account ready. If you are an individual lender, preserve transfer records, message trails, and any acknowledgment of debt. Good records reduce the drawer’s room to invent new stories later.

Important timelines you should never miss

- The cheque should be presented within its validity period.

- The legal notice must be sent within 30 days of receiving bank intimation of dishonour.

- The drawer gets 15 days from receipt of the notice to make payment.

- If no payment is made, the complaint should be filed within one month from the date the cause of action arises.

In practice, do not work on the last date. Act early. A one-day confusion on service, a holiday, an address issue, or a paperwork delay can create unnecessary risk.

What if the other side says the cheque was a security cheque

This is one of the most common defences.

People often say, “That cheque was only a security cheque, not for immediate payment.” Whether this defence succeeds depends on facts. A label alone does not automatically destroy liability. Courts examine whether a legally enforceable debt or liability existed on the relevant date.

This is where surrounding evidence becomes vital. If you have invoices, acknowledgment of outstanding amount, settlement discussion, or demand messages that line up with the cheque, the security-cheque defence becomes harder to sustain. On the other hand, if your records are vague and the cheque was issued in a more informal setting, the matter may become more contested.

This is exactly why strategic drafting and document arrangement matter from the start.

What if the cheque bounced because of stop payment or account closed

People assume that only “insufficient funds” counts. That is not the right way to think about Section 138. Dishonour reasons such as stop payment or account closed can still attract liability depending on facts, provided the statutory ingredients are otherwise satisfied and the cheque relates to a legally enforceable liability.

The larger lesson is simple. Do not self-reject your own case merely because the memo reason is not “funds insufficient.” Get the documents reviewed properly.

What if the drawer offers settlement after notice

This happens often.

After receiving a legal notice, some drawers suddenly become cooperative. They ask for a week, then two more weeks, then offer partial payment, then request instalments. Sometimes settlement is sensible. Sometimes it is a delay tactic.

Before accepting settlement, check these three things

- Does the person have a real payment plan?

- Will they sign a written settlement?

- What security do you have if they default again?

A good cheque bounce lawyer will not push every matter blindly toward trial. Sometimes the smart move is a well-drafted settlement with clear dates, default consequences, and proper acknowledgment. Sometimes the correct move is to file immediately after the legal waiting period ends.

The right answer depends on risk, amount, relationship, and prior conduct.

Civil recovery and criminal cheque bounce case: can both exist

Yes, in appropriate circumstances, a cheque bounce prosecution under Section 138 and a civil recovery action may involve overlapping facts. The Section 138 complaint addresses penal consequences arising from dishonour and non-payment after legal notice, while civil proceedings focus directly on money recovery, contractual dues, or related remedies. The legal route should be chosen based on documentation, urgency, amount involved, and overall recovery strategy.

Many claimants make the mistake of thinking there is only one remedy. In some matters, a broader strategy works better.

Practical mistakes that weaken cheque bounce cases

- Waiting too long after dishonour

- Sending an informal notice instead of a proper legal notice

- Using the wrong dates in the notice

- Demanding unrelated inflated amounts

- Losing the original cheque or memo

- Filing in the wrong jurisdiction

- Failing to prove how liability arose

- Depending only on oral understanding

- Accepting vague promises after notice without written terms

- Not tracking limitation properly

These are not technicalities in the abstract. They are real reasons why cases become difficult.

How Legals365 can help in cheque bounce matters

A cheque bounce matter is usually about money, but it is also about leverage, timing, and credibility. At Legals365, the approach is not limited to sending a notice and waiting. The team reviews whether the transaction supports Section 138, checks limitation, prepares the legal notice carefully, aligns documents, identifies the proper forum, and handles filing and prosecution support.

Legals365 already has relevant service and knowledge pages on cheque bounce notice drafting, cheque bounce legal services, and Section 138 guidance, including pages focused on notice drafting, cheque bounce legal support, and document requirements.

For clients, what matters most is that the matter gets handled properly from the start. A rushed notice with copied language often creates future damage. A carefully handled file creates pressure and keeps options open for both litigation and recovery.

Who should file quickly and not wait

Some people can afford delay. Most cannot.

- The cheque amount is large for your business cash flow

- The drawer is avoiding calls

- The drawer has issued multiple failed cheques

- The drawer is shifting addresses

- You already see a pattern of excuses

- You suspect financial distress or asset dissipation

- The relationship has clearly broken down

- The transaction record is fresh and well documented

Delay benefits the non-paying side. Action benefits the prepared side.

Realistic example 1: supplier recovery case

A packaging supplier delivers material worth Rs. 4,80,000 to a food business. The buyer issues a cheque against pending invoices. The cheque bounces. The buyer says there is a temporary cash issue and asks the supplier not to proceed legally. The supplier waits 24 days, keeps calling, gets nothing concrete, and then consults counsel.

At this stage, the matter is still salvageable, but the timeline is tight. A prompt legal notice is sent with invoice references, cheque details, return memo details, and payment demand. The buyer ignores the notice. Complaint is filed in time. After summons, the buyer proposes settlement because the file is document-heavy and difficult to dispute. This is how many practical recoveries happen.

Realistic example 2: personal loan between friends

An individual lends money to a friend over bank transfer. There is no formal agreement, but chats acknowledge the debt. The borrower later issues a cheque and asks the lender to deposit it after salary credit. The cheque bounces. The borrower then claims it was only a security cheque.

Here, message trails become crucial. If the chats clearly show the cheque was issued toward repayment, the lender’s case may still remain strong. This is why people should preserve even informal written communication.

Realistic example 3: rent default matter

A tenant issues cheque payment for rent arrears and security adjustment. The cheque bounces. The landlord is unsure whether this is only a tenancy dispute or also a cheque bounce case. If the liability is legally enforceable and the procedural steps are followed, Section 138 may still be invoked. The surrounding tenancy record, rent ledger, and communications will matter.

Is online banking replacing cheque cases completely

No. Digital payments have grown, but cheques still remain common in business, property, rent, vendor payments, settlement deals, and formal transactions. In many commercial sectors, cheques continue to act as a pressure instrument, a security mechanism, or a scheduled payment device. That is exactly why cheque bounce litigation remains active and relevant.

Why legal drafting quality matters more than people think

A badly written notice often reveals the weakness of the file. It may contain:

- Wrong cheque date

- Wrong amount

- No explanation of liability

- No proper statutory demand

- No clarity on dishonour date

- Loose allegations not backed by records

When such a notice reaches the other side, it tells them the complainant may not be fully prepared. On the other hand, a sharp notice backed by facts changes the tone immediately. It shows seriousness, awareness of law, and readiness to proceed.

That is why experienced legal drafting is not cosmetic. It is strategic.

Best Cheque Bounce Case in India: a smart filing mindset

If you truly want the Best Cheque Bounce Case in India, think like this:

- Act fast

- Document everything

- Do not overstate facts

- Send the notice correctly

- Track service properly

- File within limitation

- Choose the right court

- Prepare for defence arguments early

- Stay open to structured settlement, not vague promises

- Work with a lawyer who handles both procedure and pressure

Strong cases are rarely accidental. They are assembled with discipline.

Conclusion

Filing a cheque bounce case in India is not complicated when you understand the sequence, but it becomes risky when you delay or improvise. The core process is clear: present the cheque, collect the dishonour memo, send the legal notice within time, wait for the statutory payment period, and then file the complaint within limitation before the proper court. Under Section 138 and Section 142 of the Negotiable Instruments Act, timelines and jurisdiction are central, not optional.

For individuals and businesses, the goal is not only to start litigation. The real goal is to build a case that creates lawful pressure and improves the chances of recovery. That is what separates an ordinary matter from the Best Cheque Bounce Case in India. A well-prepared file, a properly drafted notice, and a disciplined court strategy can make a major difference.

If you are facing a dishonoured cheque and want practical legal help, Legals365 can assist with notice drafting, document review, complaint filing, strategy, and end-to-end support in cheque bounce matters. Relevant pages on the site include the cheque bounce notice service page, the broader cheque bounce lawyer page, article resources on drafting notices and document requirements, and Advocate BK Singh’s profile page.

Client Reviews

*****

Rohit Mehra

I had been chasing payment for months after a business cheque bounced. Legals365 reviewed my documents quickly, sent a proper notice, and explained every step clearly. Their handling gave me confidence from day one.

*****

Neha Arora

I was confused about whether my matter was only a money dispute or a cheque bounce case. The team at Legals365 explained the legal position in simple language and prepared the case in an organized way.

*****

Sandeep Khanna

What I liked most was that they did not give false promises. They checked the dates carefully, prepared the notice properly, and helped me understand the court filing process. Very professional support.

*****

Pooja Verma

My tenant’s cheque bounced and I had no idea what documents I should preserve. Legals365 guided me step by step and handled the matter with seriousness and clarity.

*****

Amit Bansal

I had a supplier payment issue and was worried because the other side kept delaying with excuses. After legal action through Legals365, the tone changed immediately. Their strategy was practical and effective.

*****

Shalini Gupta

The team was responsive, polite, and detail-focused. They explained timelines, notice rules, and court process without confusion. I felt the matter was in safe hands.

?FAQs

1. What is a cheque bounce case in India?

2. How many days do I get to send a legal notice after cheque bounce?

3. How much time does the drawer get after receiving the notice?

4. When should the complaint be filed in court?

5. Which court hears cheque bounce cases?

6. Is a cheque bounce case civil or criminal?

7. Can I file a case if the cheque bounced due to stop payment?

8. What documents do I need for a cheque bounce case?

9. What if the other side says the cheque was given as security?

10. Can a cheque bounce case settle after filing?

11. Can I send notice by advocate?

12. What punishment can happen in a cheque bounce case?

13. What if I missed the complaint filing deadline?

14. Can businesses also file cheque bounce cases?

15. Why should I hire a cheque bounce lawyer?

There's no reason for concern. There is no difficult-to-understand legalese.

Someone who has helped many people with the same problems gives you clear, honest advice. We want to make the legal process easy to understand and use for everyone.

+91-9625961599 Chat on WhatsAppSchedule Your Consultation