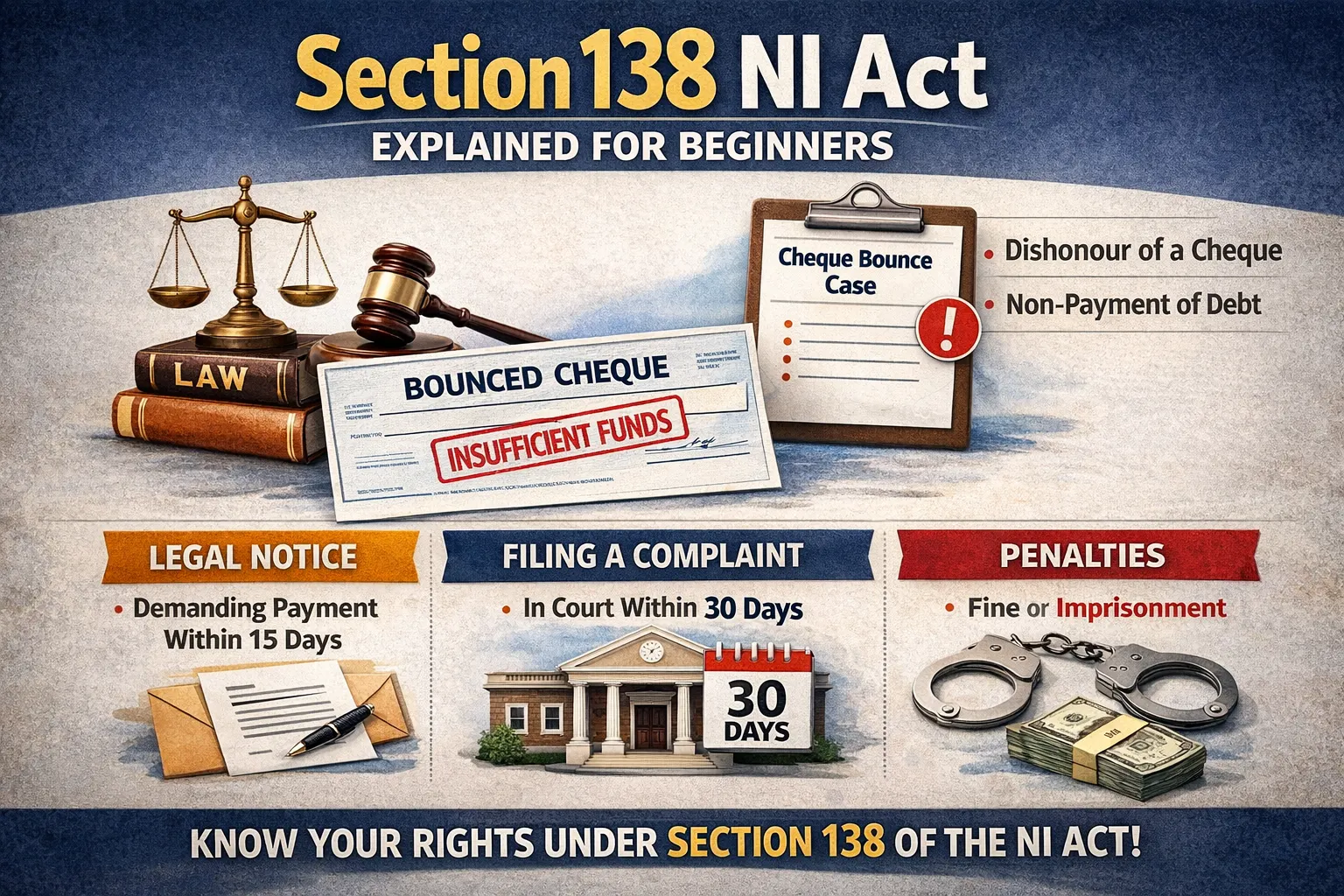

Section 138 applies when a cheque issued against a legally enforceable debt or liability is dishonoured by the bank and the legal notice procedure is properly followed. It converts a payment default through cheque into a legal issue with criminal consequences. A cheque bounce matter is not something to ignore. Delay, silence, or casual settlement discussions without proper legal advice can create serious procedural and financial problems. Early understanding helps both the payee and the drawer protect their position. Section 138 NI Act deals with cheque bounce cases. If someone issues a cheque and it gets dishonoured because of insufficient funds or similar reasons, the law may treat it as an offence. This is not merely a banking issue. It can become a criminal complaint if the statutory procedure is followed correctly. At the same time, many people dealing with loan repayment stress also look for lawful ways to stop recovery agent harassment legally in India. That concern often overlaps with cheque issues because financial distress, post dated cheques, recovery calls, and notice-based pressure can happen together. Section 138 is designed to preserve trust in cheque transactions. For the law to apply in a normal case, three points matter: In simple terms, the law does not punish every banking error. It focuses on dishonour linked to an actual liability and a properly followed legal process. A bounced cheque does not instantly become a court case. The law provides a sequence. The cheque is presented, dishonoured, followed by a written legal notice within the statutory period. The drawer then receives a final opportunity to make payment. Only after non-payment within that period does the complaint stage arise. In practice, cheque bounce disputes arise for many reasons, and not every one of them begins with a dishonest intention. Some of the most common reasons are insufficient funds, account closure, signature mismatch, presentation of a post dated cheque before its date, and technical banking issues. The legal impact depends on facts, documents, and the surrounding transaction. The possible consequences are serious. A person found guilty may face imprisonment up to two years, fine up to twice the cheque amount, or both. However, courts often encourage settlement where a practical resolution is possible. A small business owner issues a cheque of Rs. 5,00,000 to a supplier against pending dues. The cheque is deposited, but it bounces because the account does not have enough funds. The supplier sends a legal notice. If the amount is still not paid within the legal period, the supplier may file a complaint under Section 138. What began as a payment problem now becomes a criminal proceeding with financial and reputational consequences. This is why timely legal advice matters. This is one of the most misunderstood parts of cheque bounce law in India. Civil liability means the money is still due. Criminal liability under Section 138 means the law can punish the act of issuing a cheque that is dishonoured in the prescribed circumstances. Both dimensions can operate together. A person may still owe the money and also face criminal proceedings if the statutory ingredients are satisfied. Yes, the law provides for imprisonment, but jail does not happen automatically in every case. Courts generally examine conduct, payment history, defence, and settlement possibilities. Repeated default, non-appearance, evasive conduct, or a weak defence can increase the seriousness of the matter. Many people make the mistake of treating a cheque bounce notice as mere pressure. That is a risky approach. The notice is a formal legal step and also the last structured opportunity to assess the claim, verify the amount, examine the transaction, and respond in a way that protects your record. A good response may involve payment, negotiated settlement, documentary clarification, or a detailed legal reply depending on the facts. Financial disputes do not always remain limited to one legal issue. In loan-related matters, borrowers may also face aggressive recovery calls, repeated visits, or intimidation. That is why many people search for ways to stop recovery agent harassment legally in India while also trying to understand cheque bounce exposure. Recovery agents cannot lawfully threaten, abuse, shame, or disturb borrowers at unreasonable hours. Harassment can itself become a matter for complaint and legal action. Every case depends on documents and facts, but some common defence positions include proving that the cheque was issued as security, challenging the existence of a legally enforceable debt, showing that the amount was already paid, raising a signature dispute, or demonstrating misuse of the cheque. A weak oral explanation rarely helps. Proper defence usually depends on bank records, message trails, settlement history, invoices, account statements, and notice correspondence. Litigation consumes time, money, and attention. In a large number of Section 138 matters, practical settlement is more useful than prolonged contest. A structured settlement can reduce risk, preserve relationships, and close the issue before it causes wider damage. That does not mean every case should be settled blindly. It means the legal and commercial value of settlement should be assessed early. These mistakes often turn a manageable matter into a more serious legal problem. Cheque bounce disputes need practical legal judgment. A proper approach may involve notice drafting, reply strategy, limitation review, complaint filing, defence planning, settlement discussions, or recovery-related protection depending on the side you represent. Legals365 works on real case handling, practical risk review, and legally safe action. The aim is not simply to react, but to choose the correct next step based on the record. Prevention is always easier than post-default legal defence. Section 138 NI Act is about preserving trust in financial transactions. If you understand the legal sequence early, you can avoid panic, respond properly, and protect your position with more confidence. The same principle applies if you are also trying to stop recovery agent harassment legally in India. Early documentation, timely legal action, and careful response make the difference. Cheque bounce law in India may look technical at first, but once the process is explained clearly, the next step becomes easier to decide.What Section 138 Covers

Why Beginners Must Understand It Early

Understanding the Basics Before You Panic

What Exactly Is Section 138 NI Act

When Does a Cheque Bounce Become a Legal Case

Common Reasons for Cheque Bounce

Penalty Under Section 138

Real Life Example That Beginners Can Understand

Difference Between Civil Liability and Criminal Liability

Can You Go to Jail for Cheque Bounce

Legal Notice Is Not a Threat, It Is a Serious Legal Opportunity

How This Connects to Recovery Agent Harassment

Your Legal Rights Against Recovery Agents

Practical Defence Strategies in Cheque Bounce Cases

Settlement Is Often the Smartest Commercial Move

Mistakes People Commonly Make

How Legals365 Helps in Such Matters

How to Prevent Cheque Bounce Problems

Final Thoughts

Top Relevant Search Keywords

Frequently Asked Questions

Q1 What is Section 138 NI Act

Q2 Is cheque bounce a criminal offence

Q3 What is the time limit for sending a legal notice

Q4 How much time is given to make payment after notice

Q5 Can the case be settled after filing

Q6 Can a person go to jail for cheque bounce

Q7 What if the cheque was given only as security

Q8 Can recovery agents threaten or insult a borrower

Q9 How can a borrower stop recovery agent harassment legally in India

Q10 What happens if court summons are ignored

Q11 Can a Section 138 complaint be filed without legal notice

Q12 How long can a cheque bounce case take

Q13 Can company directors also be made liable

Q14 Is online filing available for cheque bounce complaints

Q15 What does fine up to twice the cheque amount mean

There's no reason for concern. There is no difficult-to-understand legalese.

Someone who has helped many people with the same problems gives you clear, honest advice. We want to make the legal process easy to understand and use for everyone.

+91-9625961599 Chat on WhatsAppSchedule Your Consultation