A recovery notice can shake even a financially disciplined person. It often arrives when income has already fallen, business cash flow has slowed, medical expenses have drained savings, or a family issue has disrupted repayments. The notice may mention an outstanding amount, legal action, or further steps. Many borrowers panic. Some ignore it. Some make rushed calls and say too much. Some start paying random amounts without securing any written protection. That is where clarity matters. The best recovery notice legal steps are not about reacting emotionally. They are about protecting your position, understanding the type of notice you have received, preserving documents, identifying legal risk, and deciding whether the matter should be answered, disputed, negotiated, settled, or defended. In many cases, the first response after receiving a recovery notice shapes how aggressively the matter moves ahead. A careful response can reduce pressure, stop procedural misuse, create room for settlement discussions, and strengthen your record if the dispute later reaches DRT, civil proceedings, or another legal forum. In India, lenders and regulated entities are expected to follow fair recovery practices. A loan settlement lawyer becomes important when the notice is not just a reminder but the start of legal pressure. That may include a recall notice, personal loan recovery notice, credit card recovery escalation, business loan default notice, SARFAESI demand notice, possession notice, auction warning, or communication from a bank panel advocate. Each type needs a different response strategy. Ignoring a recovery notice is one of the costliest mistakes borrowers make. Silence is often treated as lack of resistance or lack of a workable plan. Once that happens, the lender may move to the next stage. In secured loan matters, the process can become far more serious. A payment reminder, advocate notice, recall notice, SARFAESI demand notice, possession notice, and auction warning all carry different legal implications. Check the notice against your sanction letter, loan agreement, EMI schedule, bank statement, receipts, and prior settlement or restructuring discussions. Save the full notice, envelope, email trail, payment proof, screenshots, call logs, and all relevant records connected to the loan and recovery activity. Do not casually accept liability, promise payment dates, or confirm figures on calls before checking the account and legal position properly. A written reply creates a record, raises factual objections, requests account clarification, and opens the door to lawful negotiation or defence. You may need reply strategy, settlement support, complaint action, or urgent defence planning depending on the stage and the nature of the account. Not every recovery notice means the same thing. The language used in the document matters. A simple payment reminder is different from a loan recall notice. A lawyer notice is different from a collection message. A personal loan recovery letter is different from a SARFAESI demand notice tied to a secured asset. A possession notice is much more serious than a routine overdue notice. An auction notice requires immediate legal review. If the notice comes from a recovery agent or uses threatening language, the issue is not only repayment. It may also involve borrower rights, recovery misconduct, privacy concerns, and complaint strategy. If the notice is from an advocate on behalf of a lender, do not assume it is only pressure. It may be a pre litigation step. Many borrowers react to fear before checking whether the figures are even correct. That is risky. Sometimes the notice amount includes charges the borrower does not fully understand. Sometimes earlier payments are not properly reflected. Sometimes verbal settlement talks were never confirmed in writing. Sometimes the role of a co borrower or guarantor is not stated clearly. A salaried borrower in Noida loses a job and misses four EMIs on a personal loan. The recovery notice claims a much larger amount than expected. On review, the borrower finds bounced auto debit charges, penal interest, and legal charges. One manually paid instalment was also not clearly reflected in the account position. Without checking the ledger first, the borrower would have negotiated from a weak position. The best recovery notice legal steps always include evidence preservation. Create one physical and digital file for the entire matter. Save the notice envelope or email header, the full notice copy, loan agreement, KYC used in the account, account statements, EMI schedule, call logs, screenshots of abusive messages, field visit records, and hardship documents such as medical or business records. This record helps in three ways. It helps draft a proper reply. It helps negotiate settlement on documented grounds. It helps defend you later if the matter escalates. Borrowers often damage their own case in the first few phone calls. They say they will somehow arrange everything in two days, accept the full amount, or admit that all documents are correct. Do not make broad admissions unless you have reviewed the claim. Be polite but controlled. Ask for written communication. Say that you are reviewing the notice and will respond formally. This step is especially important where there is a dispute about interest, default date, restructuring history, co borrower liability, guarantor exposure, or the lender recovery conduct. A written reply changes the posture of the case. It shows that the borrower is not absconding. It records factual disputes. It puts hardship on record. It asks for account clarification. It resists unfair or premature recovery steps. It opens the door to lawful settlement. It also becomes useful evidence later. In many unsecured loan matters, a strong reply can push the case toward structured discussion instead of uncontrolled field pressure. You can also review related guidance through How to Respond to a Personal Loan Recovery Notice Legally and the broader Legal Process for Loan Recovery in India Explained. Borrowers often feel embarrassed to complain about harassment, but abusive recovery is not a valid substitute for legal process. You should not quietly tolerate abusive language, public shaming, repeated calls at improper hours, threats to defame you socially, unauthorised disclosure to relatives or colleagues, coercive visits, pressure to sign blank papers, or threats unrelated to lawful recovery. If this happens, complain in writing first to the lender grievance cell or nodal officer and keep proof. If the response is poor, the matter may require stronger legal escalation. If there is intimidation, trespass, or physical threat, the case may also require police complaint strategy. Not every case should be fought to the end. Not every case should be settled immediately either. A settlement may be sensible when income has fallen sharply, the account is difficult to regularise, the lender is willing to reduce the burden meaningfully, or the practical goal is controlled closure. A settlement may be risky when the lender amount is inflated, the account has legal defects, the collateral risk is immediate, or you are being pushed to pay without clear written closure terms. A loan settlement lawyer helps by negotiating the language, schedule, waiver treatment, NOC terms, and proof of closure. Many borrowers make the mistake of paying under a vague settlement discussion without securing clear written settlement conditions. You can also review the internal page on one time loan settlement with banks. A small trader in Ghaziabad receives a business loan recovery notice after months of weak receivables. The lender agent pushes for a quick lump sum. The trader borrows from relatives and pays a large amount informally. Later the lender says the money was adjusted only toward dues and not toward full settlement. This usually happens because the payment was made without a properly documented settlement letter. A secured loan notice is not the same as a credit card payment demand. If the property, machinery, vehicle, stock, or another secured asset is involved, delay becomes dangerous. The immediate tasks are to review whether the notice is legally proper, check the asset description, verify the amount claimed, preserve proof of service defects if any, and evaluate whether urgent interim protection or defence planning may be required. If you are already facing pressure linked to a home loan account, you may also review Stop Home Loan EMI Harassment for related guidance. Borrowers are often told that nothing can be done now, pay today or everything will be seized, there is no settlement option, or that once notice is issued no reply matters. These statements are often oversimplified and sometimes wrong in context. The legal effect of a notice depends on the kind of account, the stage, the documents, lender compliance, and your response. After receiving a recovery notice, the borrower usually needs one or more routes. A legal reply route works where the amount, process, or conduct needs a written response. A settlement route works where repayment failure is real and closure is the practical goal. A complaint route works where there is harassment or service deficiency. A defence route matters where secured enforcement, possession risk, or formal proceedings are approaching. A documentation route is necessary where the first need is account statement, charge breakup, or closure proof. Legals365 can support recovery notice review, dues verification, legal replies to banks and NBFCs, settlement strategy, harassment complaint preparation, pre litigation defence planning, and documentation for closure, NOC, and settlement proof. If you have received a bank or lender notice, the right question is not whether you should worry. The right question is what you should do next and in what order. The best recovery notice legal steps begin with identifying the notice type, checking the claim, preserving documents, avoiding careless admissions, sending a written reply, and choosing whether the matter should move toward settlement, complaint, or legal defence. A recovery notice does not mean you have no options. It means the matter has entered a stage where delay becomes expensive and informed action becomes valuable. If the case involves pressure, disputed dues, settlement difficulty, or asset risk, timely advice from a loan settlement lawyer can help you respond with control instead of fear. I received a recovery notice just after losing my job. Legals365 reviewed the notice, explained the next steps clearly, and helped me approach the matter with confidence instead of panic. My personal loan account was being handled very aggressively. Legals365 helped me put everything in writing and guided me on how to respond properly. That structure made a real difference. I run a small business and received a dues notice after a prolonged cash flow problem. The team explained the legal side in simple language and helped me understand what documents mattered before negotiation. What I appreciated most was that they did not rush me into random payments. They first checked the claim, discussed practical risks, and helped me think long term. I was confused between loan settlement and legal defence. Legals365 explained both routes and helped me decide what was realistic for my situation. That clarity reduced a lot of stress at home. I felt embarrassed after receiving the notice and delayed action for days. Once I spoke to Legals365, the matter finally started moving in an organized way. I wish I had taken advice earlier. Read the notice carefully, identify who issued it, verify the loan account details, and preserve all documents. Do not ignore it and do not make rushed admissions on calls. Not always. Sometimes it is a pre litigation step, sometimes a collection escalation, and sometimes part of a statutory recovery process. The legal effect depends on the notice type. In many secured recovery situations, notice based stages matter before further action. The exact legal position depends on the loan type and recovery route being used. No. Threats, public shaming, abuse, coercion, and harassment should not be treated as valid recovery methods. Such conduct should be documented and challenged properly. You can, but where the amount is high, the account is disputed, or property risk exists, a lawyer drafted reply is often safer and more effective. Yes. It should be treated seriously. Even if it is not yet a court case, it may be part of the escalation path. Consider settlement when repayment stress is genuine, the account is difficult to regularise, and the lender is open to clear written closure terms. Not blindly. First confirm how the payment will be treated and whether any settlement terms are being recorded in writing. Yes. Where there is harassment, service deficiency, or procedural misuse, complaint strategy may become an important part of the response. Ask for a statement of account, interest breakup, penalty details, and legal charges. A written objection should be considered where the calculation is disputed. A loan settlement lawyer reviews the notice, checks legal exposure, drafts replies, negotiates settlement, and helps protect the borrower from procedural mistakes. Improper and excessive calling patterns should not be accepted silently. Preserve records and seek legal guidance where the conduct becomes abusive or coercive. Treat it as urgent. If the matter is tied to a secured asset, timelines and risk stages matter much more. Yes. You can review the internal page on sending a legal notice to the bank and use that route where the matter requires a formal response. Usually no. Silence often weakens your position. A documented response is generally safer than avoidance. If you are dealing with a bank recovery notice, NBFC pressure, harassment calls, a disputed outstanding amount, or settlement difficulty, timely legal review can help you respond in a more controlled and informed way.Why this stage matters

Why You Should Never Ignore a Recovery Notice

What delay can cost you

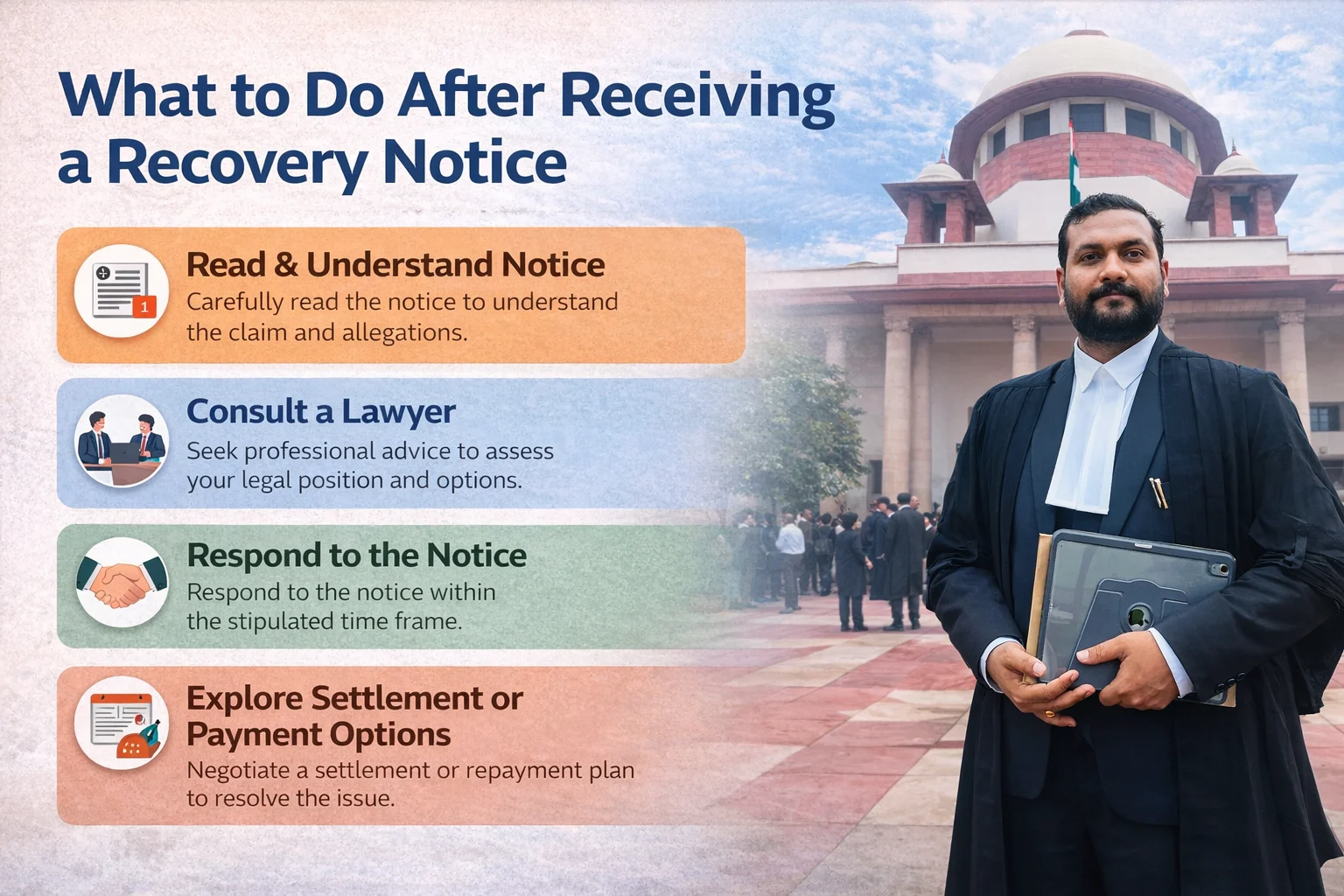

Best Recovery Notice Legal Steps After Receiving the Notice

Identify the Notice Type

Verify the Outstanding Amount

Preserve Every Document

Avoid Casual Admissions

Send a Written Reply

Choose the Right Route

Step 1 Identify Exactly What Kind of Recovery Notice You Received

Step 2 Verify the Loan Account and Claimed Outstanding Amount

Documents you should compare immediately

Practical example

Step 3 Preserve Every Document and Every Communication

Step 4 Do Not Make Casual Verbal Admissions

Important caution

Step 5 Send a Written Reply Instead of Only Emotional Calls

A good written reply should usually cover

Step 6 Understand Your Rights if Recovery Agents Are Harassing You

Step 7 Know When Settlement Is Smart and When It Is Not

Practical example

Step 8 If the Notice Involves a Secured Asset Move Fast

Step 9 Do Not Rely Only on the Call Centre Version of Events

Step 10 Choose the Right Route Reply Negotiate Complain or Defend

How Legals365 can help

Common Mistakes Borrowers Make After Receiving a Recovery Notice

Conclusion

Common Legal Queries and Terms

Explore Related Legal Services and Guidance

Client Reviews

*****

Rohit Mehra

*****

Pooja Sharma

*****

Amit Bansal

*****

Neha Verma

*****

Sandeep Yadav

*****

Kavita Arora

FAQs

Q1 What should I do first after receiving a recovery notice

Q2 Does receiving a recovery notice mean a case has already been filed against me

Q3 Can a bank recover money without sending a notice

Q4 Can recovery agents threaten or insult borrowers

Q5 Can I reply to the notice myself

Q6 Is a legal notice from a bank advocate serious

Q7 When should I consider settlement

Q8 Should I make part payment immediately to show good faith

Q9 Can I complain if the bank or NBFC behaves unfairly

Q10 What if the notice amount looks wrong

Q11 What is the role of a loan settlement lawyer in such cases

Q12 Can I be contacted at odd hours for loan recovery

Q13 What if the notice relates to home loan or property loan default

Q14 Can Legals365 help send a legal notice to the bank

Q15 Is silence ever a good strategy after receiving a recovery notice

Need Legal Guidance After a Recovery Notice

There's no reason for concern. There is no difficult-to-understand legalese.

Someone who has helped many people with the same problems gives you clear, honest advice. We want to make the legal process easy to understand and use for everyone.

+91-9625961599 Chat on WhatsAppSchedule Your Consultation