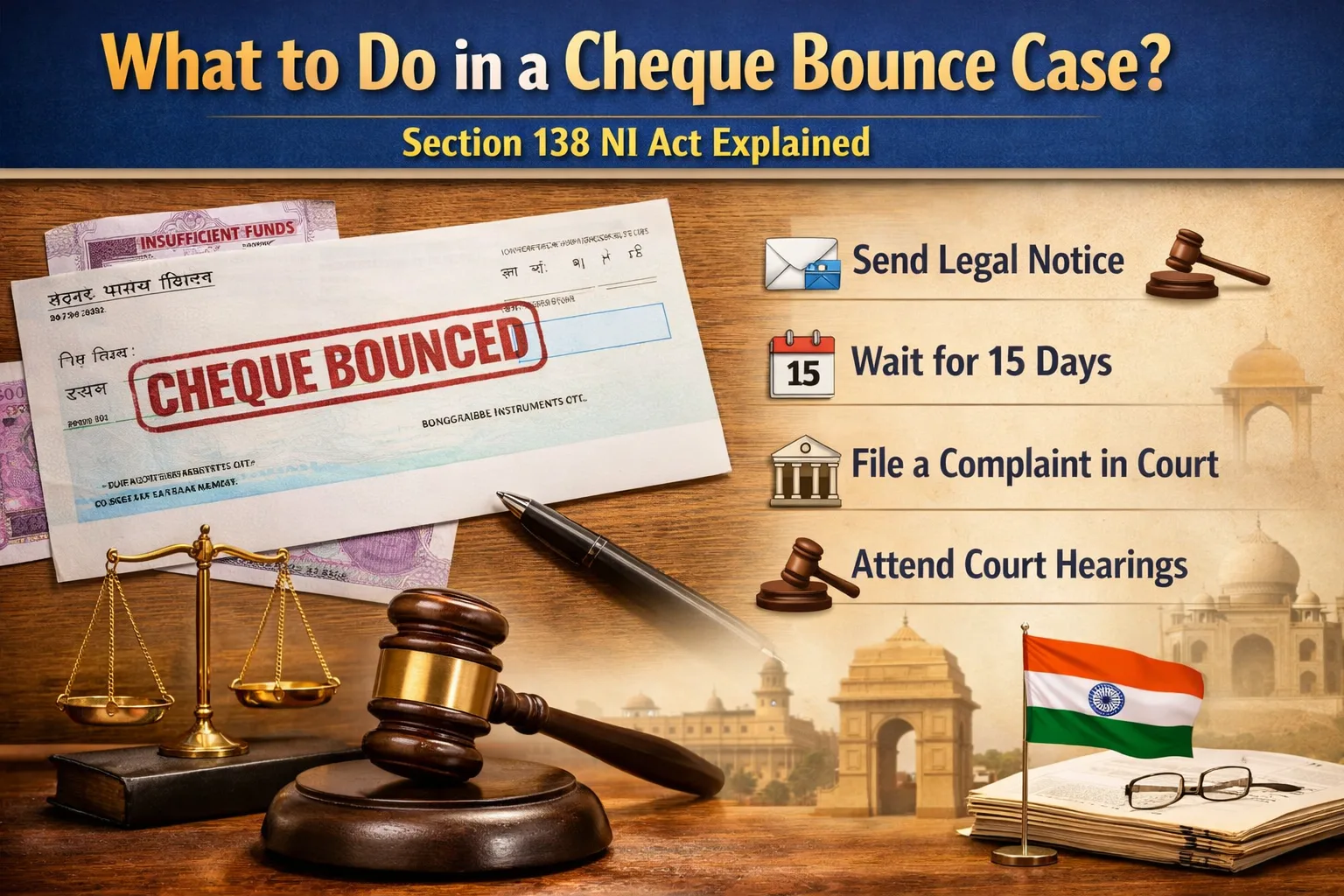

Under Section 138 of the Negotiable Instruments Act, 1881, cheque dishonour can lead to criminal prosecution if the statutory process is followed correctly. The cheque should be presented within validity, a written demand notice should be sent within the legal timeline, the drawer gets one final payment window, and only then does the complaint stage arise. A clean documentary record is often the difference between a strong case and a delayed dispute. The right answer depends on speed, documents, and timing. If you are careless with even one step, you can weaken an otherwise strong claim. If you are accused in a cheque bounce matter and you ignore the notice or the court summons, the problem can become far more expensive than the original cheque amount. That is exactly why people search for the Top cheque bounce case guidance online. They do not just want legal theory. They want a practical route they can actually follow. A cheque bounce lawyer becomes especially valuable because cheque bounce cases look simple from the outside, but they are full of technical timelines, documentary requirements, presumptions, and tactical choices. If you want a practical overview from a broader legal support platform, you may also review Section 138 NI Act explained for beginners. This guide explains what to do whether you are the payee trying to recover money or the drawer trying to defend yourself legally and intelligently. Many people think a dishonoured cheque is just a payment delay. In practice, it can trigger legal notice, criminal complaint, appearance before a Magistrate, interim compensation applications, settlement pressure, and business reputation damage. For a supplier, a bounced cheque can disturb cash flow. For a landlord, it can mean missed rent and a longer dispute. For a lender, it may be the first sign that recovery will not happen voluntarily. For the person who issued the cheque, the problem is not limited to one dishonour. Once notice arrives, every response matters. A lot of mistakes happen in the first ten days after dishonour. People misplace the return memo. They do not preserve courier proof. They send the wrong notice. They assume WhatsApp messages are enough. They wait too long because the other side promises next week. Then limitation becomes a fight of its own. That is why the Top cheque bounce case approach is not aggressive for the sake of it. It is disciplined. It focuses on building a clean legal record from day one. Section 138 applies when a cheque drawn by a person on an account maintained by them is returned unpaid for insufficiency of funds or because it exceeds the arrangement made with the bank, and the statutory requirements are later fulfilled. The offence is not complete on dishonour alone. The legal sequence includes drawing of cheque, presentation, dishonour, written demand notice, and failure to pay within 15 days of receipt of notice. If these stages are mishandled, the complainant may lose procedural advantage. If they are handled well, the case becomes substantially stronger. If you need process support for the notice stage, you can compare that with cheque bounce notice legal service guidance. People often assume only one reason matters, namely insufficient funds. In reality, returned cheques may come with various remarks. Some reasons help the complainant more clearly than others, and some reasons create factual disputes. Not every dishonour automatically leads to conviction, but many returned cheque situations still support a Section 138 complaint if the legal ingredients are present and the cheque was issued toward an enforceable liability. If you deposited a cheque and the bank returned it unpaid, do not jump directly into emotional calls or threats. First, build your legal file. A proper Section 138 notice is not a casual complaint letter. It should clearly set out the facts and demand payment within 15 days of receipt. A strong notice usually contains the name and address of both parties, cheque number, date, amount, bank details, date of presentation and dishonour, reason for return, legal background of liability, and a clear demand to pay within the statutory window. The notice should also be sent properly. Courier proof, speed post receipt, tracking report, email trail if used additionally, and address accuracy all matter. For a separate practical note on drafting, you may see how a legal notice for cheque bounce should be drafted. After the notice is received, the drawer gets 15 days to make payment. If payment is made within that period, the criminal cause of action under Section 138 does not mature. If no payment is made within those 15 days, the complainant can file the complaint within the next one month under Section 142. This phase is often decisive because one of three things usually happens. The drawer pays in full. The parties negotiate a settlement. The complainant moves to complaint filing. Many cheque disputes end in negotiated closure once the notice makes the risk real. Others do not move at all until a court summons is served. Jurisdiction was a major issue in cheque bounce litigation, but Section 142(2) now gives a statutory rule. If the cheque is delivered for collection through an account, the case is generally filed where the payee's bank branch is situated. If it is presented otherwise through an account, the place may shift to the drawer's bank branch. This matters more than people think. Filing in the wrong place can delay the matter, create objections, and waste time. If a company is prosecuting the case, authorization and board-related paperwork should be prepared properly. If the cheque was issued by a company, the question of who signed, who was in charge, and who can be arrayed as accused becomes important under Section 141. Once the complaint is filed, the Magistrate examines the complaint and supporting material. If satisfied, the court may issue summons. People searching for the Top cheque bounce case route usually want faster recovery. In real life, speed depends on court workload, service of summons, cooperation of parties, quality of record, and whether settlement remains possible. Let us make it practical. Do not rely only on verbal promises. Preserve tenancy record, rent ledger, bounced cheque, notice, and any admission by the tenant. If multiple months are due, strategy becomes important because you may have cheque bounce, rent recovery, eviction, and civil consequences operating together. Friendly loan cases are common but often poorly documented. Save the transfer proof, chat history, loan acknowledgment, witness support if any, and details of why the cheque was issued. The other side may later say it was a security cheque or was issued without liability. Keep invoices, delivery proofs, ledger statements, GST records where applicable, email approval trail, purchase order, and any balance confirmation. Commercial records make these cases significantly stronger. For document-side preparation, you may also compare this with documents required to prove a cheque bounce case in court. Settlement cheques are especially sensitive because parties often assume the dispute is over. If the settlement amount itself bounces, move quickly and preserve the settlement agreement. In all these situations, the safest route is disciplined paperwork and timely legal action, not anger-led messaging. A lot of accused persons worsen their position by staying silent. Silence is rarely a strategy. A thoughtful reply notice can be useful in the right case. It may set up your defence early. In other cases, direct settlement may be the better path. But ignoring a valid notice is often costly. Not every defence succeeds, and courts examine facts closely. Still, these are common areas where disputes arise. The legal presumption under Section 139 is important here. The law presumes in favour of the holder that the cheque was issued toward debt or liability unless the accused rebuts that presumption. This is why defence in a cheque bounce matter is not about broad denial alone. It requires documentary rebuttal, cross-examination planning, and consistency. This is one of the most overused phrases in cheque bounce litigation. Many accused say, it was only a security cheque. But that label by itself does not end the case. Courts look at whether a liability existed when the cheque was presented and whether the cheque was connected to a subsisting obligation. If you are the complainant, do not panic merely because the other side says security cheque. Focus on showing the actual debt, transaction history, and why the cheque was rightly presented. If you are the accused, do not assume the phrase alone will save you. You need context, documents, and a coherent factual story. In many cases, yes. Section 138 prosecution is one remedy. Separate civil recovery action may also be available depending on facts. The strategic choice depends on amount, urgency, limitation, solvency of the other side, and settlement possibility. Some clients want only pressure for payment. Some want a court-recognised recovery route. Some need both leverage and money decree options. A skilled cheque bounce lawyer will usually assess what combination best serves the client. Section 143A allows the court, in certain circumstances, to direct interim compensation up to 20 percent of the cheque amount during the pendency of the case. This is not automatic in every case. This matters because many accused persons assume they can simply contest for years without financial pressure. That is no longer always realistic. For complainants, a properly argued interim compensation application can be useful in the right file. Section 148 empowers the appellate court, in appeal against conviction, to order deposit of at least 20 percent of the fine or compensation awarded by the trial court, subject to the statutory scheme and judicial interpretation. In practical terms, conviction does not mean a cost-free appeal. Settlement is common and often sensible. A good settlement should be written clearly. It should mention total amount, schedule, default clause, mode of payment, and legal consequences of breach. Do not settle casually on phone calls alone. In many real files, the best outcome is not the most dramatic order. It is a legally secured payment plan that actually gets completed. A supplier delivers packaged goods worth Rs. 4,80,000. The retailer issues two cheques. One clears, one bounces. The supplier has invoice set, delivery proof, ledger confirmation, and return memo. Notice goes in time. The retailer keeps asking for ten more days but never pays. Complaint is filed in proper jurisdiction. This is usually a structurally strong complainant file. What makes it strong is not only the bounced cheque. It is the transaction record behind it. A person transfers Rs. 3,00,000 to an acquaintance over bank transfer and later receives a cheque. The cheque bounces. The accused claims it was a blank signed cheque misused and that the transfer was investment, not loan. Now messages, call records, and exact wording in chats become crucial. Friendly loan cases are winnable, but only if the factual trail is coherent. Two parties have a larger commercial dispute. They sign a written settlement and issue a cheque toward settlement amount. The cheque bounces. Here, the settlement document itself may become the backbone of the complainant's case. This is often cleaner than older disputed invoice chains because liability has been freshly acknowledged. Do not choose only on aggressive promises. A cheque bounce lawyer should be able to tell you, after seeing your papers, where your case is strong, where it is weak, and what immediate step cannot be delayed. For service-side reference, you may also see cheque bounce lawyers in Delhi. People often ask whether Section 138 guarantees recovery. No lawyer should promise that. But a strong case can create serious legal pressure and often improves chances of settlement or court relief. The best legal strategy depends on whether your real aim is quick payment, strong defence, commercial closure, or long-term enforcement. In cheque disputes, angry conversations make people feel active, but documents win cases. The complainant who preserves papers, dates, and notices properly is usually ahead. The accused who responds early, organizes records, and avoids inconsistent statements is also ahead. A cheque bounce case is often won or lost before the first serious hearing, because that is when the factual foundation is already fixed. This is how ordinary cheque disputes become legally credible claims instead of messy payment quarrels. For a stepwise overview, you can also see how to file a cheque bounce case in India. A bad defence is often worse than an early negotiated settlement. If the factual issue concerns delay or response handling, you may compare it with what to do when facing a cheque bounce notice. A cheque bounce matter under Section 138 NI Act is technical, time-bound, and deeply fact-sensitive. The law gives the payee a strong remedy, but only when the statutory steps are followed properly. It also gives the accused meaningful defence opportunities, but only when those defences are raised intelligently and backed by real material. So, if you are facing a bounced cheque, do not treat it as a minor banking inconvenience. Treat it as a legal file from the first day. That is the difference between confusion and control. That is also why many clients looking for the Top cheque bounce case solution turn to an experienced cheque bounce lawyer who can handle notice, complaint, defence, settlement, and courtroom strategy with precision. If you want a broader legal support resource, you may also review a complete guide to cheque bounce cases in India. Below are high-intent cheque bounce search themes relevant to this article. Each link is used only once. Collect the cheque return memo, preserve the cheque and transaction documents, and calculate limitation immediately. The next major step is issuing a proper legal notice within 30 days of receiving information about dishonour. No. The cheque should generally relate to a legally enforceable debt or liability, and the statutory process must also be followed correctly. The payee must issue the written demand notice within 30 days from receiving bank intimation of dishonour. The drawer gets 15 days from receipt of the notice to make payment. After the 15-day payment period expires, the complaint is to be filed within one month from the date cause of action arises under Section 142. In many standard cases where the cheque is presented through the payee's bank account, jurisdiction lies where the payee's bank branch is situated under Section 142(2). Possibly, depending on whether a legally enforceable liability existed when the cheque was presented. The word security alone does not decide the case. Section 139 creates a presumption in favour of the holder, but the accused can try to rebut it with credible evidence. Yes, and in appropriate cases persons responsible for the company's conduct may also be implicated under Section 141, depending on facts and pleadings. Yes. Section 143A allows interim compensation up to 20 percent in the statutory framework, but it is discretionary and not automatic in every case. Yes. Many cheque bounce cases settle even after summons or during trial. In many situations, yes. Civil remedies and Section 138 proceedings can coexist, subject to facts and strategy. You should still take immediate legal advice. Ignoring notice does not make the matter disappear and may worsen your position once the complaint is filed. Not always. Speed depends on court workload, service of summons, documentary clarity, and settlement possibility. Section 143 provides for summary trial, but actual timelines vary. Because notice drafting, limitation, jurisdiction, rebuttal of presumptions, documentary strategy, settlement drafting, and court handling all require precision. A mistake in the early stage can affect the entire case.Quick Legal Position

Why a Cheque Bounce Case Becomes Serious So Quickly

What Section 138 of the NI Act Actually Covers

Core Legal Elements Usually Required

Common Reasons for Cheque Bounce

Common Return Reasons

Other Disputed Reasons

First Steps if You Received a Bounced Cheque

What a Valid Legal Notice Should Contain

Notice Checklist

What Happens After the Legal Notice

Where to File the Complaint

What Documents Are Usually Filed With the Complaint

Typical Complaint Filing Set

Court Process After Filing a Cheque Bounce Complaint

Initial Stages

Trial Stages

If You Are the Complainant, What Should You Actually Do?

Situation 1: A tenant gave you a rent cheque and it bounced

Situation 2: A friend returned part of a personal loan by cheque and it bounced

Situation 3: A business client paid for supplied goods by cheque and it bounced

Situation 4: You settled a dispute and the settlement cheque bounced

If You Are the Accused Drawer, What Should You Do?

Immediate Response Steps for the Accused

Common Defence Points in Section 138 Matters

Security Cheque Defence: When It Works and When It Fails

Can You File Both Civil and Criminal Proceedings?

Interim Compensation and Why Accused Persons Should Take It Seriously

Deposit During Appeal After Conviction

Settlement in Cheque Bounce Cases

When Settlement Usually Makes Sense

Practical Mistakes That Weaken a Complainant's Case

Practical Mistakes That Weaken an Accused Person's Defence

Realistic Example 1: Supplier Versus Retailer

Realistic Example 2: Friendly Loan Dispute

Realistic Example 3: Business Settlement Cheque

How to Choose the Right Cheque Bounce Lawyer

What Outcome Can You Expect in a Cheque Bounce Case?

Possible Outcomes

Why Documentation Matters More Than Anger

The Top Cheque Bounce Case Strategy for Complainants

The Top Cheque Bounce Case Strategy for Accused Persons

Final Word

Relevant Search Keywords Covered in This Blog

?FAQs

Q1. What should I do first after a cheque bounces?

Q2. Is every bounced cheque a Section 138 case?

Q3. How many days do I get to send a legal notice?

Q4. How much time does the drawer get to pay after receiving notice?

Q5. When can I file the complaint in court?

Q6. Where should a cheque bounce complaint be filed?

Q7. Can I file a case if the cheque was given as security?

Q8. What if the accused says there was no debt?

Q9. Can a company be made accused in a cheque bounce case?

Q10. Can the court order interim compensation?

Q11. Can the matter be settled after the case is filed?

Q12. Can I also file a civil recovery case?

Q13. What if I ignored the legal notice?

Q14. Is a cheque bounce case always fast?

Q15. Why should I hire a cheque bounce lawyer?

There's no reason for concern. There is no difficult-to-understand legalese.

Someone who has helped many people with the same problems gives you clear, honest advice. We want to make the legal process easy to understand and use for everyone.

+91-9625961599 Chat on WhatsAppSchedule Your Consultation