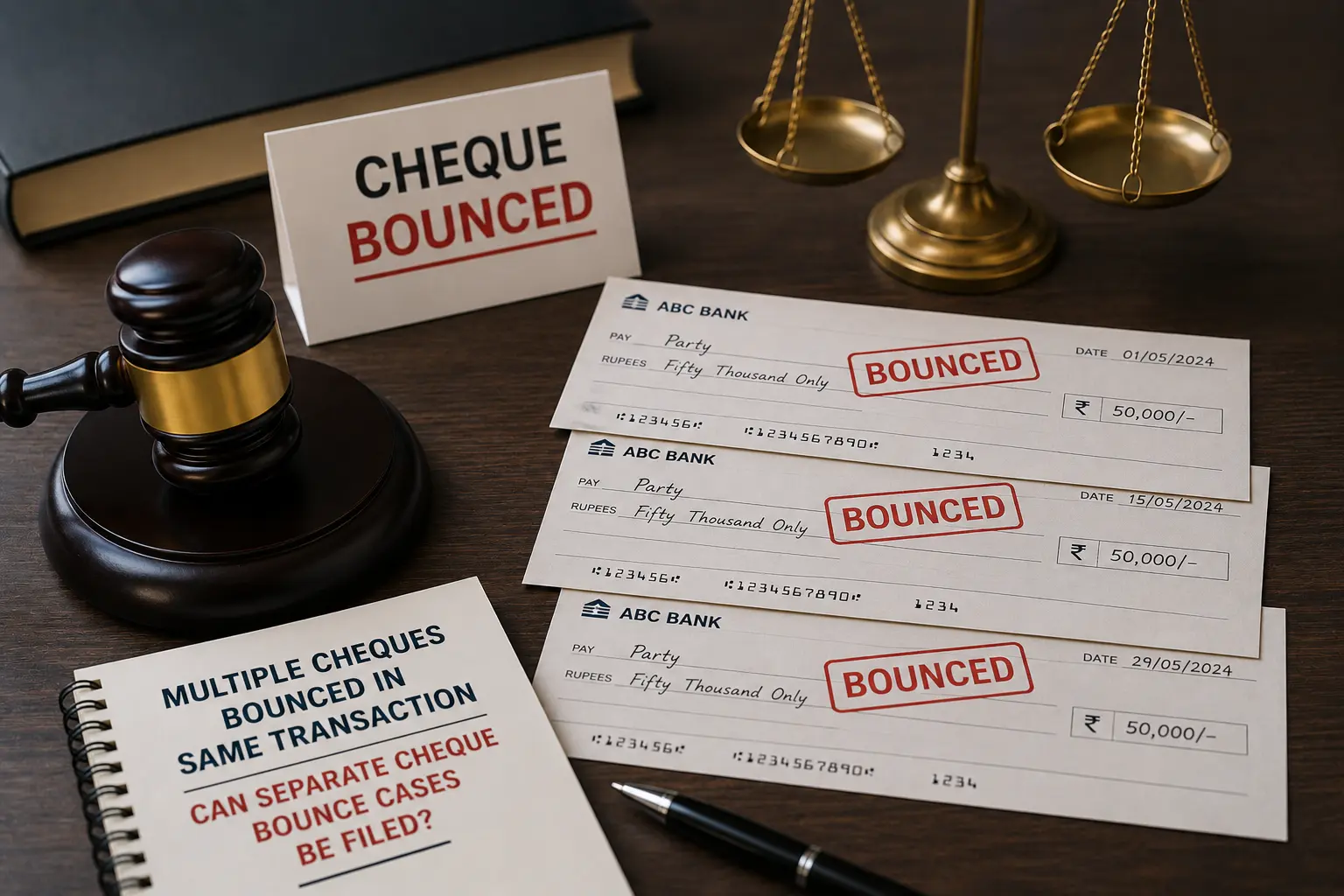

Cheque Bounce Law Guide 2026 Cheque bounce cases are normally straightforward: the cheque got presented, was dishonoured, you issued statutory notice, they did not pay within 15 days, so the law allows you to file a complaint. But then clients come with more complicated situations: multiple cheques were issued in the same business deal. Later all or some cheques bounce and the customer asks: Should I send one notice or many? Should I file one case or separate cases? As a lawyer handling bounced cheque litigation since 2008, Advocate BK Singh gets these questions often in Delhi NCR, Ghaziabad, Noida, Gurugram, Faridabad, Meerut, Lucknow and other Indian cities. The reality is these situations happen everywhere. Builders issue many refund cheques to buyers. Business vendors get multiple cheques against one supply order. Borrowers issue cheques towards different portions of principal, interest, late fees. Sometimes companies pay from their account and personal guarantors issue cheques independently as “support” or “backup”. Can separate cheque bounce cases be filed under these circumstances? This guide tries to answer that question in detail. Cheque bounce cases in India have evolved over two decades from an informal recovery tactic to a detailed statutory process. In 2026 every stage of a cheque bounce case is watched carefully by courts, including limitation, jurisdiction, contents of the statutory notice, proof of liability, documentary evidence, digital evidence, company liability and dual complaints for same cheques. Clients from Delhi NCR and adjoining commercial belts like Ghaziabad, Noida, Greater Noida, Gurugram and Faridabad see multiple cheques commonly in property transactions, car or bike dealership payments, transport business contracts, supply-chain credit transactions, friendly loans and business dispute settlements. Mumbai, Pune, Bengaluru, Hyderabad, Chennai, Kolkata, Ahmedabad and other Indian cities have similar trading patterns. The consequences are not only for the complainant side. Accused persons also get multiple summons, bail applications, trial dates, interim compensation requests and social stigma. In serious commercial disputes, the accused may face repeated court appearances, compensation or deposit-related orders where applicable, settlement pressure and reputational concerns, but account freezing is not an automatic consequence of a Section 138 NI Act complaint. If the cheques are issued by a company or firm, the signatory and those persons who were in charge of and responsible for the conduct of business may face proceedings under Section 141 NI Act, depending on specific allegations and facts. No side should take an undisciplined approach. The payee or holder should ensure proper notice and avoid excessive demands in pleadings. But drawers and account holders should also not send rash replies like “All cheques were part of same transaction, so no court case can be separately sustained.” Such statements do not hold good after the latest 2026 Supreme Court ruling. Anyone who has received two or more cheque bounce summons can benefit from an early discussion with Advocate BK Singh. He can quickly review whether separate cases are legally valid, whether a combined complaint has merits or whether settlement or compounding is advisable before emotional trial pressure escalates. Section 138 NI Act applies when cheque “is returned by the bank unpaid”. Main reasons include insufficient funds, exceeds arrangement, stopped payment and other legally recognized return reasons depending on facts. Section 138 requires that a cheque is presented, dishonoured, notice served and final payment not made. Each dishonoured cheque can create separate cause of action if these steps are complete. Same transaction does not automatically bar multiple cheque bounce cases. Keep cheque specifics in mind. Limitation for Notice under Section 138 NI Act is usually 30 days from bank information on cheque dishonour. Drawer has 15 days to make payment from the date of notice receipt. For jurisdiction of Complaint, see Section 142 NI Act. Cheque bounce cases are usually filed where payee’s bank branch is located if the cheque was deposited in holder’s bank account. Cheque bounce cases can be compounded or settled between the parties. But any agreed amount should be clearly documented. Indian law focuses on the cheque, but also examines the debt underlying the cheque. Can multiple cheque bounce complaints arise against the same person if all cheques relate to one transaction? In most situations, yes. Each cheque is a promise to pay on demand. Legal pros also say: the root cause of issuing multiple cheques does become relevant in law. For readers who prefer simple definitions: A multiple cheque bounce is when two or more cheques are issued by a drawer in connection with one business deal, loan advance or personal transaction. All the cheques bounce when presented for payment and the payee wants to initiate legal action under Section 138 NI Act. Courts look at objective evidence. Did the drawer issue each cheque towards a debt he was bound to pay? Was each cheque valid when presented to the bank? Did the bank return each cheque unpaid? Was sufficient notice given? Did the drawer fail to make payment within the notice period? If yes, the law allows one cause of action per dishonoured cheque. The defences around “same transaction” are still valid in limited facts. Cheques which were clearly issued as alternative, fresh or replacement instruments can be argued as one transaction. Has the borrower repaid the loan after giving one cheque? Were multiple cheques issued for different portions of principal, interest and late fees? Did the seller return some cheques after receiving payment from a third party? Were cheques deposited despite clear promise of full payment by other means? Those facts can all be legally relevant, but they usually require proof. Documentary abuse should stand out from the notice pleading or admitted documents. The takeaway lesson for someone who has just received multiple cheque bounce summons is this: Do not jump to conclusions that the cases are bogus or fatally flawed. For someone holding multiple cheques know that just because you have multiple bounced cheques, the law does not automatically allow you to file 10 separate complaints. Each cheque’s facts should be examined on its own merit. The law that applies to cheque bounce complaints is Chapter XVII of the Negotiable Instruments Act, 1881 (“NI Act”). Specifically: If the cheque was issued by a “company”, “firm” or “business concern”, then Section 141 becomes relevant. Company directors and partners can become accused in a cheque bounce case, but certain conditions apply. A person should not be named as accused just because they are a company director or recipient of notices. Section 143A allows interim compensation in a pending cheque bounce case. Section 148 talks about deposit of cheque amount on appellate stage after conviction. Section 147 allows complainants to compound the offence even after filing a complaint. Most important for this guide is the Supreme Court decision in Sumit Bansal v. M/s MGI Developers and Promoters, 2026 INSC 40. The Supreme Court explained that one underlying transaction does not automatically merge multiple cheque dishonours into one single cause of action. If each cheque is a distinct instrument and the statutory sequence of presentation, dishonour, notice and failure to pay is complete, separate Section 138 NI Act proceedings may be maintainable. However, whether cheques were issued as alternative, replacement, security or supplementary instruments can still be examined on facts during trial. Quashing of a Section 138 NI Act complaint is not done by a civil court. Depending on the date and procedural position of the case, older matters may refer to Section 482 CrPC, while post-BNSS proceedings may refer to Section 528 BNSS. BNSS generally came into force on 1 July 2024, and Section 528 preserves the High Court’s inherent power to prevent abuse of process and secure the ends of justice. Keep these points in mind when reading actual court judgements. The law allows multiple cheque bounce cases to be filed in genuine situations. The defenses for “same transaction” still exist, but they have to be raised clearly. Merely mentioning “all cheques were for the same business transaction” may not be enough. Lawyers know that every case should be judged on its own facts. There is no shortcut to understanding multiple cheque bounce scenarios. Advocate BK Singh reviews each cheque’s dates and documents before suggesting filing, defending, settling or quashing action. People get multiple cheques for many reasons. Businesses receive cheques against bulk payments from regular customers. Builders issue many cheques to property buyers as part of refund. Landlords accept cheque from tenants for arrears. Suppliers allow purchasers to pay by cheque after delivering goods on credit. Car loan agents issue cheques to borrowers after receiving EMI instalments. Lawyers receive multiple cheques from clients as stage-wise fees. Company accounts see the same practice. A vendor may issue five cheques towards one invoice series. A distributor may issue dated cheques for stock supplied in one month. A dealership may issue staggered cheques under one purchase deal. Issuing multiple cheques does not become illegal, but the filing route depends on actual facts and documents. Even defendants require this guidance. Sometimes drawer issues multiple cheques as security to a lender. Or they may send replacement cheques upon customer request. Sometimes debtor issues cheques anticipating insurance recovery or third-party contribution. The Indian law does not reward casual drafting by either side. Defences like full-payment, no-liability, invalid notice or wrongful jurisdiction are fact-dependent. Issues like material cheque alteration, stolen cheque, signing authority or misuse after settlement also become relevant. Individuals and families face such problems in friendly loans. A person may give three cheques after borrowing money from family or friends. Later, the relationship sours. All cheques may be deposited on impulse without notice. These cases require objective review. Don’t fall into emotional biases during cheque bounce litigation. If you haven’t filed any case yet, readers may benefit from our guide on How to File a Cheque Bounce Case in India. Before filing any cheque bounce complaint, try collecting all evidence before acting. Don’t send one standard notice for all cheques without verifying dates. Each cheque bounce process starts from the bank return memo date. Try mapping every cheque separately on a whiteboard. Note cheque numbers, dates, bank branches, amounts, cheque presentation dates, return dates by bank and final notice deadline. Send Section 138 Notice carefully. One notice can cover multiple cheques if clearly mentioned. Keep records of posting or online notice. Different cheques can also be covered in separate notices. Mismatch in notice drafting will give the other side an excuse. Drawer has 15 days to pay after notice. If he does, you may not have a Section 138 complaint anymore. If drawer does not pay within the notice period, the cause of action arises for each cheque. Complaint must be filed within the prescribed period. Complaint drafting and court-fee payment are technical tasks. A lawyer can ensure the complaint includes legally enforceable liability, cheque issuance, presentation, dishonour, statutory notice and services, cheque amounts and proper court. After filing, the complaint is scrutinised by the Judicial Magistrate. If the prima facie case is made out, summons are issued and the accused has to enter defence. Cheque bounce complaints can be settled or compounded at many stages. However, the settlement agreement must clearly mention the total amount due, payment terms, breach consequences and terms of withdrawal or compounding along with pending court cases. Readers in Delhi and NCR can refer to Cheque Bounce Lawyers in Delhi if their matter falls under Delhi jurisdiction. As per Section 138 NI Act, the prosecution case is built on documents. Oral assertions are not enough. Courts insist on paperwork. Collect every cheque, bank’s return memo, deposit slip, account statement, invoice or agreement for the buyer. Do not file without confirming dates and details. Is it a property refund? Get the allotment letter, agreement to sell and builder receipts. Copy of cancellation and refund promise also become relevant. Is it a business supply transaction? Preserve purchase orders, delivery challans, tax invoices, ledger and bank statements. Do not forget email acknowledgements of dues. Remember, drawer side documents also matter. Obtain receipts if you’ve made part-payment. Do not hesitate to demand refund vouchers. Get bank records if you’ve paid by cheque or online. Wrongly issued cheques, misuse after loan repayment or issuance as “security” are facts provable on documents. Avoid answering the Section 138 notice emotionally without consulting a lawyer. See this useful guide on How to Reply to a Section 138 Cheque Bounce Notice in India. Law respects time in cheque bounce cases. Courts punish delay. Remember these timelines: Multiple cheques require separate verification. One cheque’s notice and bank memo may be within time. But what about the second and third cheques? Did you receive notice or were some notices returned? Don’t rush drafting the complaint. Real-world delays are common. Cheque bounce summons are served late. Drawer changes address to avoid summons. Company records need to be checked for legitimacy. Cheque bounce matters get transferred due to jurisdiction issues. Settlement discussions confuse parties emotionally. But they don’t stop limitation from running automatically. Delhi NCR courts receive huge volumes of cheque bounce cases. Ghaziabad, Noida, Gurugram, Faridabad, Meerut and Lucknow see similar high numbers. Cheque bounce lawyers here know that poor documentation causes repeated adjournments. Once notices are sent, decide quickly whether to issue a single combined notice or send separate notices. If you are the drawer or accused, quickly decide if you will pay or not, reply or not, settle or negotiate or strictly defend. Ignoring the notice and hoping problems will go away is the worst strategy. Read our detailed guide on Cheque Bounce 2026: Section 138 Notice, Timeline & SC Direction for more information on due dates. If you are drawer of multiple cheques, ignoring court summons can result in multiple complaints. You will get separate summons for each complaint. You will have to apply for bail separately. You will have to deal with evidence and potentially settlement discussions separately. If you are employer or a company facing multiple bounced cheque complaints, pending Section 138 cases can damage your reputation. Suppliers, investors, family members and vendors may think you do not honour payment obligations. For wrongful accusations against company directors, there can be personal harassment even if the transaction was for genuine commercial purposes. If you are the complainant and ignore the bank’s deadlines, your entire case gets weak just because you filed the notice or complaint beyond the prescribed time. Defective drafting by the lawyer can also cause objections, adjournments and unnecessary hearings. Emotional trauma is something that people ignore at their own risk. Lawyers often see clients only when they are desperate. Cheques got issued years ago. Holder lost papers. Family convinced them to file. Someone promised quick settlement. After some time, the very same family member or friend asks you to avoid court. These are real-life examples. Take legally advised action early. Advocate BK Singh advises clients to review their options before losing patience: Check limitation. Check the correct forum for filing. See whether cases can settle or not. Don’t go to court unless the cheque cases are worth the time, cost and litigation risk. Consult a lawyer immediately if more than one cheque has bounced from the same party, especially if the amounts are high or the transaction involves property, business supply, company accounts or settlement documents. Legal advice is also needed if you received multiple notices for the same underlying debt. Do not rely on internet templates. Your defence may depend on whether the cheques were issued as security, replacement, guarantee, part payment or full repayment. A lawyer should review the matter if the cheque was issued by a company, partnership firm, proprietorship concern or authorised signatory. Section 141 liability needs careful handling. Directors who were not involved may have separate legal remedies. You should also consult a lawyer before making payment after notice. Payment wording matters. A badly written payment message may be treated as admission beyond what you intended. For clients who want a measured view, Advocate BK Singh can assess whether the case should be filed, defended, settled, compounded or challenged before the High Court in appropriate circumstances. Legals365 assists clients in cheque bounce matters across India, including Delhi NCR, Delhi, New Delhi, Ghaziabad, Noida, Greater Noida, Gurugram, Faridabad, Meerut, Hapur, Lucknow, Jaipur, Mumbai, Pune, Bengaluru, Hyderabad, Chennai, Kolkata, Ahmedabad and other major cities. The first step is document review. The team checks every cheque, return memo, notice, service proof and transaction record. Then the case is mapped cheque-wise so the legal position becomes clear. For complainants, Legals365 can help with notice drafting, complaint preparation, court filing support, evidence arrangement, settlement strategy and representation coordination. For accused persons, the team can help with notice reply, defence review, quashing assessment, settlement negotiation and compounding documentation. Advocate BK Singh focuses on practical legal advice, not false assurance. Some cases deserve strong filing. Some deserve settlement. Some need careful defence because the complaint may be defective. That judgment comes only after reviewing facts. Readers may visit Legals365 for legal service information and consultation options. Yes, separate cheque bounce cases can be filed if each cheque has independently completed the Section 138 NI Act requirements. The cheque must be presented, dishonoured, followed by valid notice and remain unpaid after the 15-day period. Same transaction alone does not automatically prevent separate cases. One debt may still be supported by multiple cheques. Courts examine whether each cheque was a distinct instrument and whether each dishonour created a separate statutory cause. If the cheques were merely alternate or replacement instruments, the accused may raise that defence with evidence. Yes, one notice may cover multiple bounced cheques if all details are clear and the notice is within limitation for each cheque. It should mention cheque number, date, amount, bank, dishonour date and return reason. Poor drafting can create avoidable disputes. In some situations, one complaint may include multiple cheques, especially where they relate closely and the notice is common. Yet separate complaints may also be legally maintainable depending on facts. Advocate BK Singh can review whether one complaint or separate complaints are better. Quashing is possible only in limited cases. The High Court may interfere where the complaint is clearly defective, barred, abusive or unsupported by basic ingredients. Disputed facts like payment, security cheque or alternative cheque usually require trial evidence. A security cheque can still attract Section 138 if a legally enforceable debt or liability existed when the cheque was presented. The word “security” alone does not end the case. The accused must show facts and documents supporting the defence. Each cheque must be checked separately. Notice is generally sent within 30 days from bank information of dishonour. The drawer gets 15 days after receiving notice. Complaint filing usually follows within one month after cause of action arises. Yes. Section 147 NI Act makes cheque bounce offences compoundable. Parties can settle after notice, after filing, during trial or even at later stages, subject to court procedure. Settlement terms should be written clearly to avoid fresh disputes. Directors can be made accused only if the complaint meets Section 141 requirements. The signatory is usually directly involved, but non-signatory directors need specific role-based allegations. Casually adding every director may invite legal challenge. Yes. A notice reply can shape the future defence. Advocate BK Singh can help examine whether the cheques were issued for liability, security, settlement, guarantee or replacement, and whether payment or settlement should be offered. Multiple Cheques Bounced in Same Transaction: Can Separate Cheque Bounce Cases Be Filed? In most legally valid situations, yes, provided every cheque satisfies the Section 138 NI Act requirements. The safer answer is not based on emotion. It is based on cheque-wise facts. For complainants, the message is to act within limitation and draft carefully. For accused persons, the message is to respond with documents, not anger. Same transaction is a relevant fact, but it is not a complete defence by itself. Advocate BK Singh and Legals365 can help clients evaluate filing, defence, settlement and compounding options in multiple cheque bounce matters across India. Early legal review usually saves time, money and avoidable court complications. Disclaimer: This article is for general legal information only and does not constitute legal advice.Multiple Cheques Bounced in Same Transaction: Can Separate Cheque Bounce Cases Be Filed?

Why This Issue Matters in India in 2026

Quick Facts Box

Understanding the Core Legal Issue

The Legal Framework

Important 2026 Supreme Court Update

Who Needs This Guidance?

What Is the Step-by-Step Process?

Documents and Evidence Checklist

Timelines, Practical Delays and Decision Windows

Common Mistakes People Make

Risks of Ignoring the Matter

When Should You Consult a Lawyer?

How Legals365 Can Help

Frequently Asked Questions

1. Can separate cheque bounce cases be filed for multiple cheques from the same transaction?

2. What if all cheques were issued for one debt?

3. Can one legal notice cover multiple bounced cheques?

4. Can one complaint include many cheques?

5. Can the accused get multiple cheque bounce cases quashed?

6. Is a security cheque covered under Section 138 NI Act?

7. What is the limitation period in multiple cheque bounce cases?

8. Can cheque bounce cases be settled after filing?

9. Can company directors be made accused in multiple cheque bounce cases?

10. Should I contact a lawyer before replying to a multiple cheque bounce notice?

Final Thoughts

There's no reason for concern. There is no difficult-to-understand legalese.

Someone who has helped many people with the same problems gives you clear, honest advice. We want to make the legal process easy to understand and use for everyone.

+91-9625961599 Chat on WhatsAppSchedule Your Consultation